High car prices, loan rates fueling an affordability crisis in the auto industry

Canva

High car prices, loan rates fueling an affordability crisis in the auto industry

Two new cars parked outside an auto dealership.

Automobiles were far from the only commodity that saw a dramatic rise in cost in 2022, with historic inflation affecting nearly every sector of the economy. However, a perfect storm of ballooning costs and increasing auto loan interest rates has resulted in an affordability crisis that is putting pressure on both the auto industry and individual consumers.

To understand why buying a car has never been less affordable, Automoblog compiled data from industry sources including the Cox Automotive/Moody’s Vehicle Affordability Index (VAI), which measures the relative affordability of an average new car in terms of how many weeks of an average family income it would take to buy the car.

Over the past two years, the VAI hasn’t just increased, it’s done so exponentially. From January 2012 through August 2021, the VAI hovered between 32 and 36. Following that period, however, the VAI began a steep increase, reaching 43.6 in the most recent report from Cox. This figure is an all-time high, meaning cars are less affordable than ever before.

![]()

Automoblog

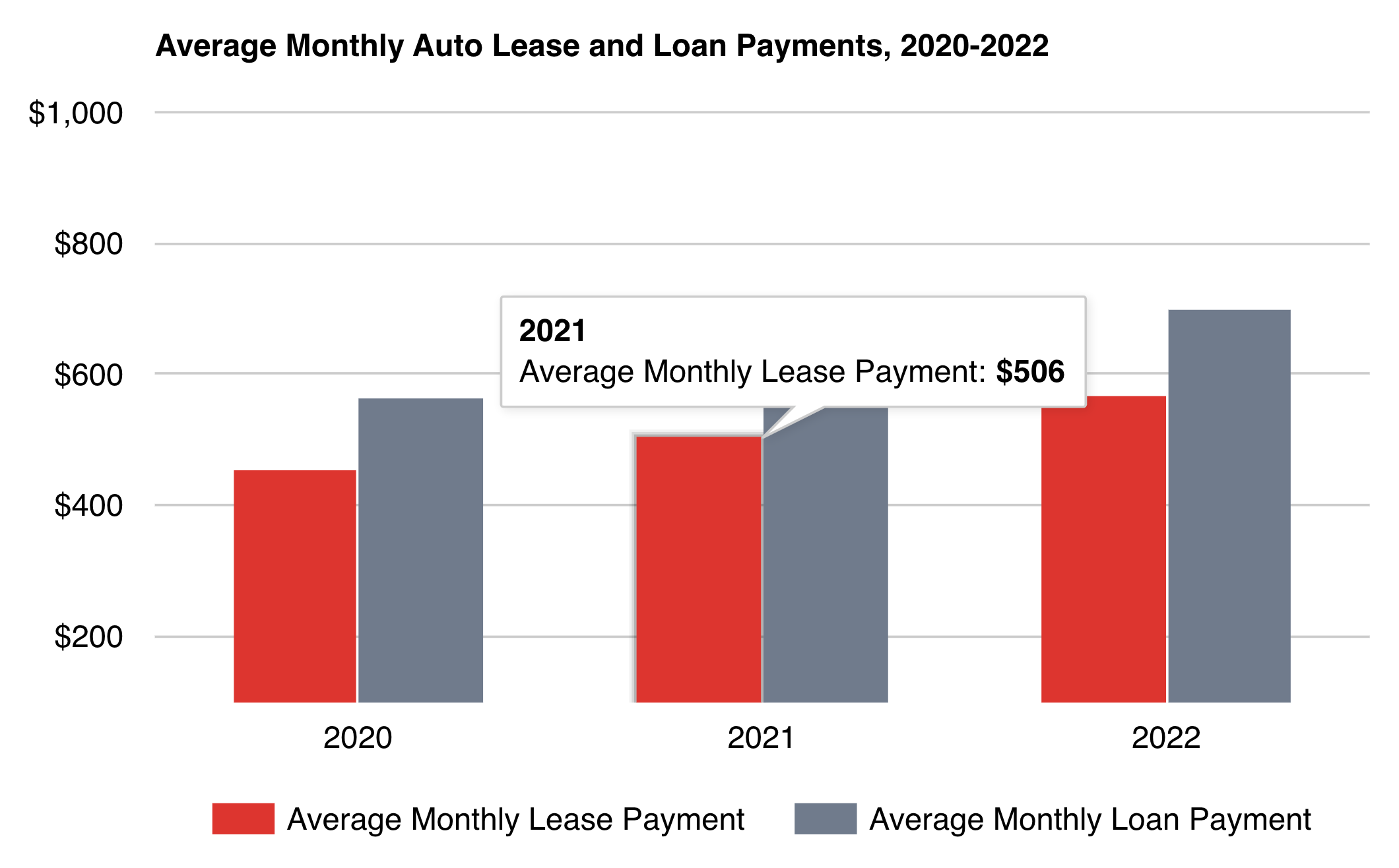

Average Car Payments Have Increased Sharply

Bar chart showing average monthly auto lease and loan payments from 2020 to 2022.

According to the Experian State of the Automotive Finance Market Q3 2022 released in December 2022, individual new car payments are also at a record high – both for leases and loan payments.

The report states that the average lease payment in Q3 of 2022 was $567 per month. This is a 12.1% increase over the average monthly lease payment of $506 in Q3 of 2021. As for loan payments, they reached an average of $700 per month in Q3 2022. This represents a 13.3% increase over Q3 2021. It’s also a historic high.

Both figures mean that the cost of keeping a car has grown significantly over the last year. Car payments have increased at an even higher rate than general inflation rates during the same period – a period in which the inflation rate was the highest it has been in over 40 years.

Despite Falling Wholesale Values, Used Car Prices Remain High

While used cars come with a lower sticker price when compared with new cars in general, the data from the State of the Automotive Finance Market Q3 2022 shows increases in used-car payments that are similar to those for new cars.

And although wholesale prices for used cars started to come down towards the end of 2022, those prices have not yet translated to lower consumer prices. Despite the marked decrease, used car prices remain at an all-time high.

Automoblog

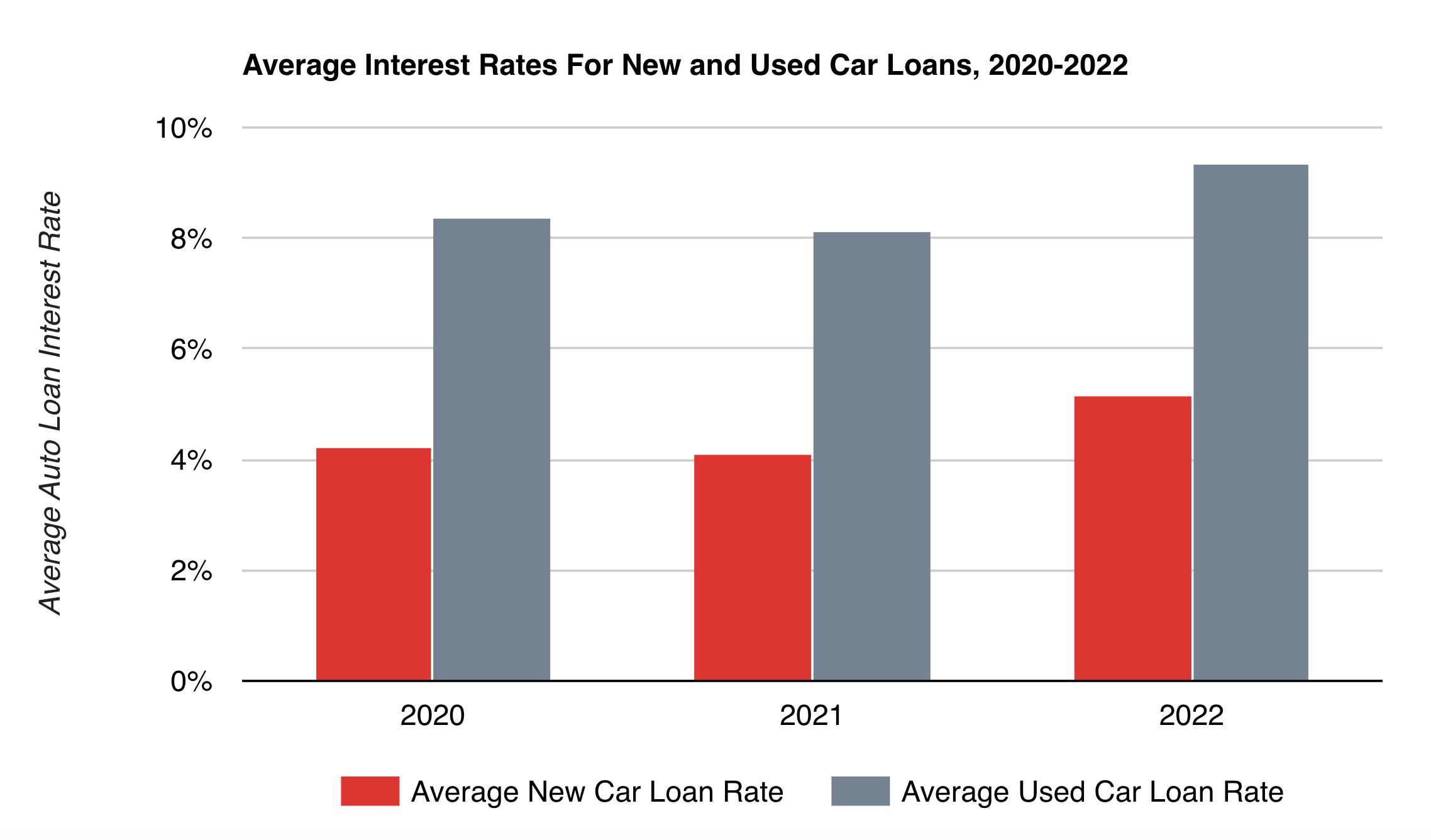

Interest Rates Have Risen Dramatically

Bar chart of average interest rates for new and used car loans from 2020 to 2022.

Another factor that has added to the cost of buying a car is the significant increase in auto loan rates over the past year. Spurred by multiple increases to the federal funds rate, automotive loan interest rates have grown even more quickly by percentage than car payments over the last year.

The average interest rate for used cars grew from 8.12% to 9.34% between Q3 2021 and Q3 2022, an increase of 15.02%. When it comes to new cars, the average interest rate grew from 4.09% to 5.16% during that same period, an increase of more than 26% on the year.

These increases mean that on top of historically-high prices for new and used cars, people have to pay significantly more to borrow the money to buy them.

Automoblog

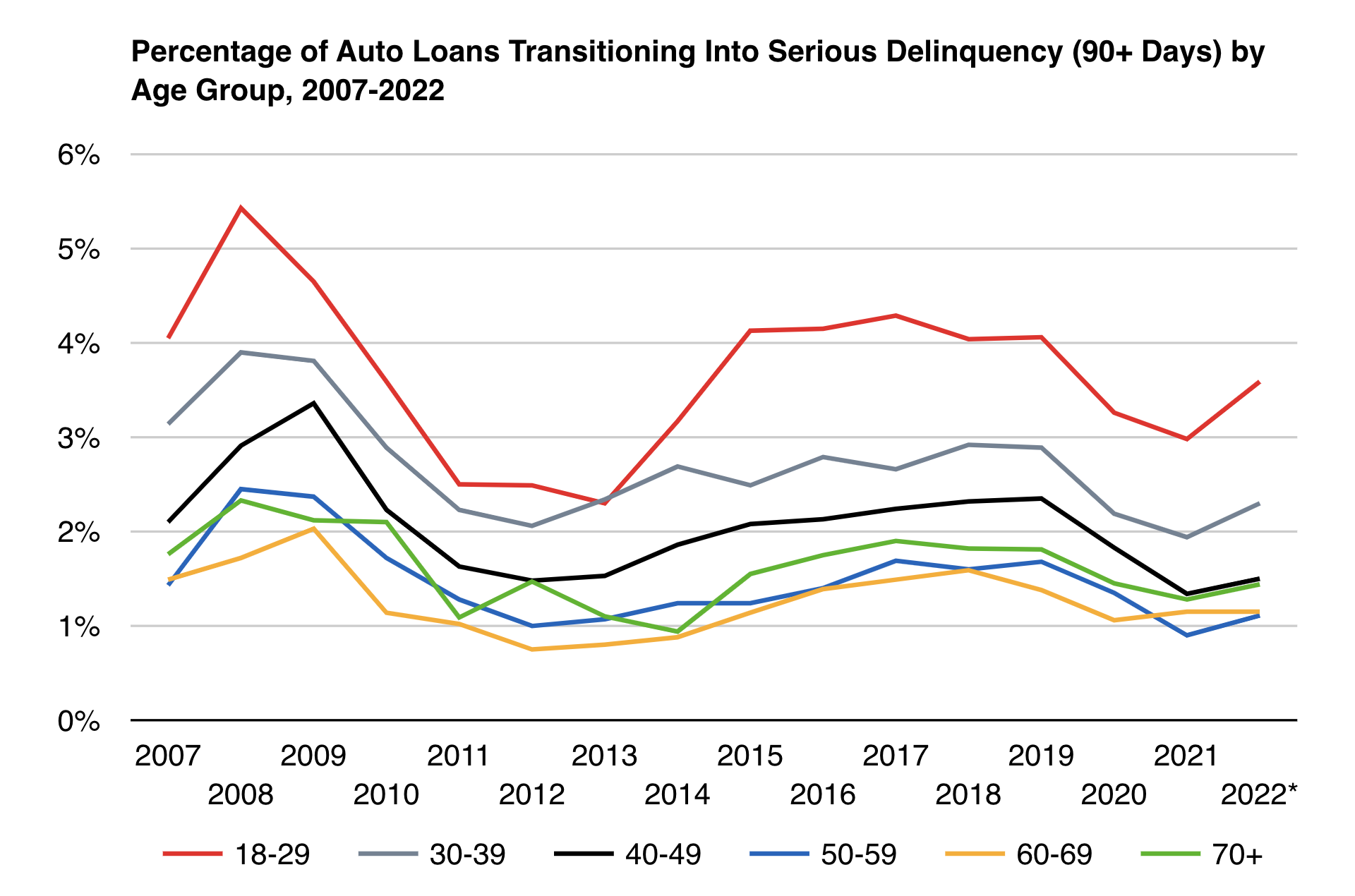

Auto Loan Default Rates Continue to Climb

Line chart showing percentage of auto loans transitioning into serious delinquency by age group from 2007 to 2022.

News emerged in mid-2022 that auto loan default rates had started to rise, especially among younger generations. Since then, default rates have only continued to increase.

Younger age groups are still the most heavily affected. In 2022, data from the Federal Reserve Bank of New York (also known as the New York Fed) revealed that 3.59% of auto loans held by borrowers aged 18-29 were headed into serious delinquency, which is defined as payments being 90 or more days late. That figure reached 2.3% for borrowers between the ages of 30 and 39.

In fact, auto loan delinquency rates rose in 2022 for every age group except for borrowers aged 60 to 69. Delinquency rates rose to an average of 1.85% across all age groups – a 16% increase from 2021.

Low-Income and Low-Credit Borrowers Are the Hardest Hit

While delinquencies and other effects of rising costs and rates have impacted nearly all segments of borrowers, it has been borrowers with lower incomes and lower credit scores that have seen the most acute effects.

Automoblog spoke with Andy Arledge, Associate Executive Vice President of the North Carolina State Employees’ Credit Union (SECU) Consumer Lending division, about these effects from the lender’s perspective.

Arledge explained that SECU has seen a reduction in loan applications and originations in recent months, along with an increase in delinquencies. A drop in loan applications and originations signifies a decrease in demand, while a rise in delinquencies indicates that borrowers are having a harder time meeting their payment obligations.

“We have experienced a slight decrease in application and origination volume, which has been across all credit score tiers,” said Arledge. “However, borrowers with lower income and lower credit scores have experienced higher delinquency and charge-off rates, as expected.”

Rising Costs of Living Have Eaten Into Family Budgets

The increase in the price of vehicles and auto loan rates is only part of the reason for the increase in delinquency rates, according to Arledge.

“Delinquency and charge-offs have increased over the last few months,” he said. “Several reasons likely contribute to this, including the rate increases. But also, a large factor is the inflation rate, which has resulted in increased costs for consumer goods and services.”

According to data from the Bureau of Labor Statistics (BLS), overall inflation hit a 40-plus-year high of 7.1% in 2022, with the costs of goods and services rising in every sector. Food costs rose 10.6% in 2022, and energy costs climbed by 13.1%.

These cost-of-living increases were not met with an equivalent increase in wages. The Conference Board estimates that the U.S. median wage rose by around 3.6% in 2022.

As a result, individuals and families had to increase their expenditures on necessities at a far higher rate than their wages increased. This left the average American with much less room in the budget for car payments and other expenses.

Canva

Auto Loan Rates Will Likely Continue to Rise In 2023

A row of brand new cars in different colors of the same make.

There are myriad factors that make changes to the cost of new and used vehicles difficult to predict. Ongoing supply chain issues and chip shortages are two such factors that may continue to limit the supply of new vehicles, which could in turn keep consumer prices from falling.

But even if the price of cars does come down, the cost of borrowing money to buy one isn’t likely to do so in 2023. Arledge says that his division at SECU expects “that auto loan rates will continue to rise in the coming year.”

This expectation is in line with public messaging from the Federal Reserve about planned rate increases over the next year. The organization released a Summary of Economic Projections report on December 14, 2022 that projects further increases to the current federal funds rate of 4.25-4.5%. The report suggests that the rate could rise to as high as 5.1-5.4% in 2023. This will likely translate into even higher interest rates on auto loans.

Experts Advise Borrowers To Be Cautious With Car Loans in 2023

Individual and even corporate car buyers have no control over the external factors that are driving the current affordability crisis. Increases to interest rates are all but guaranteed over the next year. And even if the price of new and used cars does start to come down, it will only be doing so from historic highs.

With that in mind, Arledge says that people who borrow money to buy cars in 2023 should exercise caution. One of the most important ways to do so, he says, is to consider all aspects of a vehicle loan carefully before agreeing to one.

“All borrowers, regardless of credit or income, are encouraged to shop for the best rate and terms available,” he said. “Borrowers are often misled by the payment amount only, and don’t consider the actual rate and terms to which they are agreeing. This results in higher interest costs and longer loan terms.”

“Additionally, borrowers should be mindful that used vehicle values are decreasing,” said Arledge. “They should consider the loan to value [ratio] when entering into a vehicle loan agreement.”

The current slight value downturn could continue or even intensify, potentially leaving borrowers with a vehicle that’s worth much less than they paid for it. For some, this could lead to owing more money on a car than it’s worth, even if they had positive equity at the time of the loan.

Canva

High Car Prices and Auto Loan Rates Could Continue Into 2023 and Perhaps Even Further

Three new cars are parked inside an auto dealership.

If the last several years have revealed anything about the automotive industry, it’s that predictions about the direction it’s headed in are just that – predictions. Industry researchers and insiders may have insight into numbers about investments, interest rates, and more, but it has become abundantly clear that the industry is vulnerable to countless factors from around the globe.

The following year could bring stability to the automotive supply chain and an improvement in the chip shortage. Decreased demand in the market could drive prices down and make vehicles more affordable, even with higher interest rates. However, rapidly-changing geopolitical situations, looming threats of recessions, and other unforeseen circumstances could just as easily worsen the current status quo.

In the meantime, people in the U.S. and elsewhere will have to continue to battle record-high costs and interest rates if they want to buy a car – or even keep the one they have. And while everyone is at the mercy of the automotive market, the financial market, and the economy at large, those with lower incomes and credit profiles will bear the brunt of them all.

This story originally appeared on Automoblog and has been independently reviewed to meet journalistic standards.