India reached 100B digital payments in 2023: Could it work in the US?

Nattakorn_Maneerat // Shutterstock

India reached 100B digital payments in 2023: Could it work in the US?

Customer using phone for payment via a QR code.

The National Payments Corporation of India introduced a digital public infrastructure project called Unified Payments Interface in April 2016, which has helped the country attain digital sovereignty by reducing its dependence on foreign service providers for digital payments. Uniqode used NPCI data to explore the growth of the country’s UPI.

UPI allows users to send and receive money instantly at no charge via bank accounts, virtual payment addresses, smartphone apps, or a combination of biometrics and an Aadhaar, a 12-digit identification number.

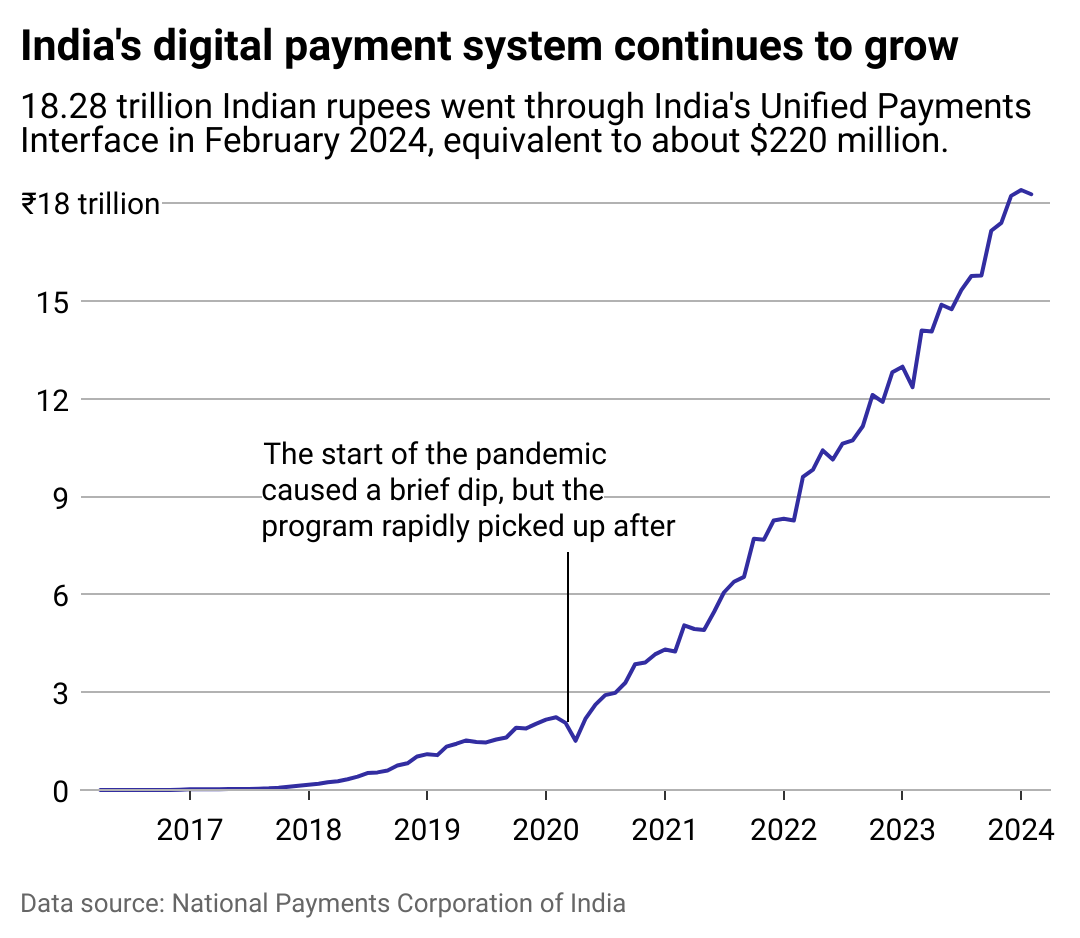

UPI’s primary objective was to turn India into a digital economy, reducing—if not eliminating—the need for paper currency. UPI transactions crossed the 100 billion mark in 2023, with the number of transactions increasing by nearly half that year. The payment system is projected to surpass such rivals as Mastercard and Visa in India, which, thanks to UPI, had the highest number of real-time payment transactions globally in 2022.

UPI has bolstered financial inclusion in the country, empowering millions of previously unbanked communities and individuals nationwide to access financial services and make transactions.

From street vendors to grocers, small businesses can settle accounts with customers digitally and securely without the customer or vendor having to divulge confidential banking information like credit card details or account numbers.

Every UPI user can create a Virtual Payment Address (username@bankname), an identifier that helps users send and receive money without sharing private information. Users can safely share their VPA with peers to receive money. Alternatively, using a UPI service provider app, customers can scan a dynamic or static QR code shared by the merchant or another user to pay for products and services. Users without smartphones can also use UPI to make payments using their unique Aadhaar and biometrics.

![]()

Uniqode

A rapid expansion

Line graph showing the growth of India’s digital payment system, which exceeded 18.28 trillion rupees in February 2024.

UPI has had a significant impact on India’s economic growth, helping the Indian economy save about $67 billion since April 2016, according to a 2023 World Economic Forum report. The technology helps small businesses by reducing transaction costs and bolstering operational efficiency and cash flow. UPI also opens small businesses to a broader customer base due to its accessibility to those who prefer not to carry around cash.

About half of the payments made via UPI can be categorized as small payments, such as a cup of milk tea worth 10 cents or a $2 bag of vegetables. With no minimum transaction amount, customers and merchants can use the technology for various microtransactions and macrotransactions.

Speaking to the Times in 2023, Dilip Asbe, the managing director and CEO of the NPCI, said as of that year approximately 300 million individuals and 50 million merchants used UPI for sending and receiving money.

During the COVID-19 pandemic, the Indian government used UPI to send financial aid to nearly 200 individuals.

India has also worked to export the technology to other countries. In 2023, Bhutan and Nepal started facilitating transactions through UPI. During the February G20 summit that year, Indian Prime Minister Narendra Modi expressed India’s willingness to assist other countries with setting up their own similar payment systems.

Nonresident Indians living in Australia, Canada, Hong Kong, Oman, Qatar, Saudi Arabia, the United States, the United Arab Emirates, and the United Kingdom started using the technology in 2023 on their international phone numbers. In February 2024, merchants in France began accepting UPI—including at the Eiffel Tower.

GaudiLab // Shutterstock

The US approach

Two young female professionals using cell phones to send payment.

Zelle, Venmo, and Cash App are common peer-to-peer and peer-to-merchant payment methods in the U.S. similar to UPI.

Venmo and Cash App are similar to UPI in that users can create usernames they can share to send and receive money instead of account and routing numbers. Both apps also allow users to scan QR codes to transact.

Unlike UPI, however, these services don’t allow instant deposits of money directly into someone else’s bank account. In terms of instant bank account deposits, Zelle is the U.S. payment service most similar to the UPI. Although Zelle doesn’t use QR codes or usernames, one can use their phone number or email to send and receive money.

Unlike the UPI, these services are private initiatives and do not run on public digital infrastructure. Sending money through wire or the automated clearing house system takes about one to three business days in the U.S.

In 2023, the Federal Reserve announced its new instant payments infrastructure, FedNow, was live and accessible to participating financial institutions. Like Zelle, the FedNow service processes and settles transactions instantly, allowing funds to be sent and received quickly. Like UPI, customers cannot directly access FedNow; instead, they can access the service through fintech platforms and banks that subscribe to FedNow as their digital highway for transactions.

FedNow is more similar to India’s real-time gross settlement system than the UPI in that it lacks any analog to the virtual payment address. QR codes cannot be used to make or receive payments. Instead, customers must use their account and routing numbers to send and receive money.

FedNow faces competition from The Clearing House’s RTP, or real-time payments network, first made available to participant financial institutions in 2017. As the FedNow program struggles to attract new participant institutions, it has also sparked interest in the RTP network. The Clearing House is a private association of federally insured banks; unlike FedNow, the service is not public infrastructure.

UPI’s global reach, and whether countries like the U.S. will adopt it, is still unpredictable—but UPI undeniably stands to influence the global digital payment landscape for years to come.

Story editing by Nicole Caldwell. Copy editing by Paris Close. Photo selection by Clarese Moller.

This story originally appeared on Uniqode and was produced and

distributed in partnership with Stacker Studio.