Small banks emerge as the top source for small business financing

Canva

Small banks emerge as the top source for small business financing

A Black woman at the desk is showing an application document to an African American woman sitting opposite her.

When it comes to borrowing money, small businesses are most likely to apply at large banks. But they often find success with their counterparts in the finance world: small banks.

Small banks—or those with less than $10 billion in total assets—comprise most of the banks in the U.S., much like small businesses account for nearly all U.S. businesses. More than 80% of small businesses that applied for financing at small banks were at least partially approved in 2022, according to data from the Fed’s most recent survey of small business employers. However, only 30% of small businesses applied at small banks when they sought financing.

About 2 in 5 small business employers applied for some traditional financing in 2022. Most needed the money to meet operating expenses, while a little over half sought cash to expand their operations.

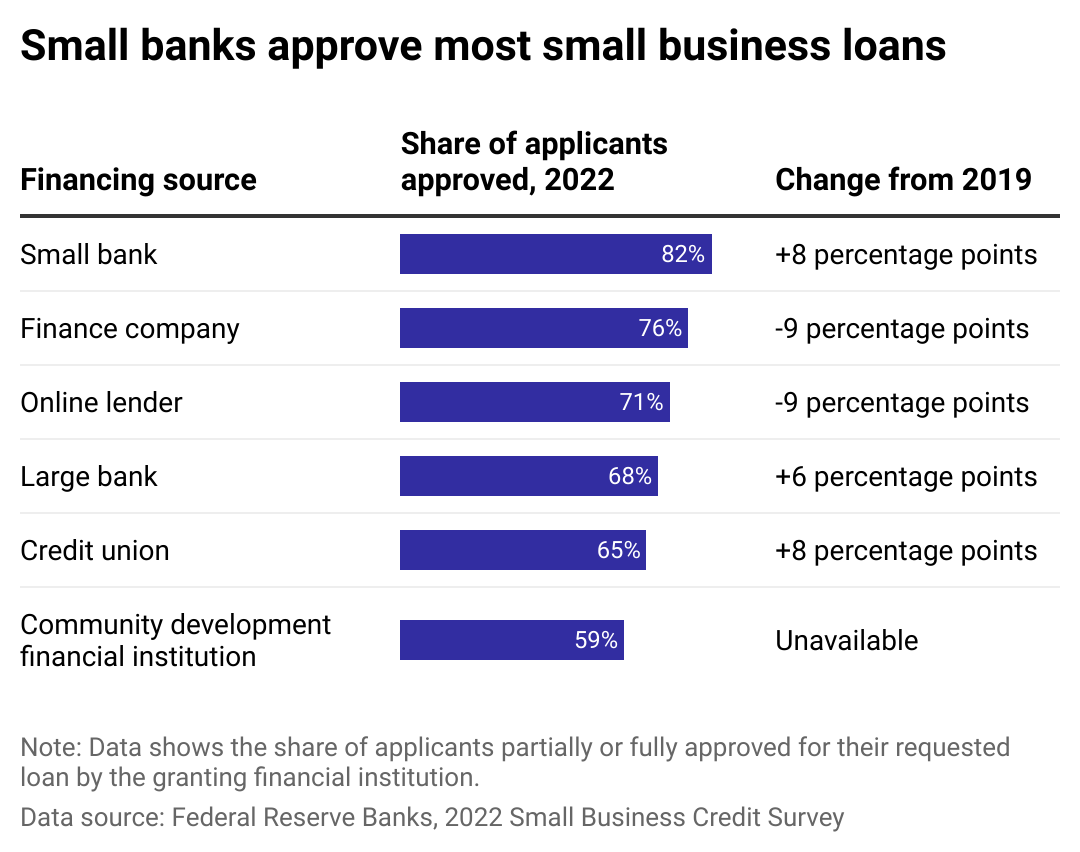

Findbusinesses4sale used the Fed’s Small Business Credit Survey data to compare approval rates among small business financing sources, taking a closer look at their differences. Approval rates are based on applications for loans, credit, and cash advances at the various institution types. The Fed report was released in March 2023 based on a 2022 survey of nearly 8,000 small businesses with employees.

![]()

Findbusinesses4sale

Small banks surpass online lenders, finance companies in approval rates for small business applicants

A bar chart shows the share of small business applicants at least partially approved for loan requests, separated by the type of source applied to.

Also known as community banks, small banks are well-equipped to lend to small businesses because of their intimate knowledge of local economies. Small businesses are often young, with short histories, small operations, little collateral, and unproven financial success. These factors can make it difficult for founders to qualify for credit and loans—they’re simply a riskier investment for a funder to take on.

Small banks’ decision-makers live within the same areas where they grant loans, and they have insight into how certain businesses could fare within their neighborhoods. That makes it easier for them to analyze the risk of lending to small businesses and, in turn, decide whether to approve their applications. At least 3 in 5 (61%) applicants considered to be a medium or high credit risk were approved for financing at small banks; at large banks, not even half (45%) of these riskier applicants were approved.

By operating across smaller locales, community bank operators also have the opportunity to forge stronger relationships with business founders. The Fed survey shows that about 2 in 3 small businesses that applied for financing with these banks did so because of an existing relationship. Many of these relationships were forged in the heat of the COVID-19 pandemic, when community banks came through for small businesses with relief funds, including more intensive support in understanding and completing complex applications.

Small firms applying to other sources, such as online lenders and finance companies, are most often motivated by making quick decisions and perceiving that they have a higher chance of being approved. That was the case five years ago, but approval rates for both sources lagged behind small banks in 2022. Indeed, approval rates at both have fallen significantly since 2019, while approvals at small banks have grown.

Both online lenders and finance companies still approve slightly higher shares of applicants with medium to high credit risks compared to small banks, but only by a few percentage points. At the same time, many more borrowers reported dissatisfaction and challenges working with these lenders, including high interest rates and unfavorable repayment terms.

On the other hand, the vast majority of borrowers from small banks were happy with their experience—much more than those who borrowed from any other type of lender.

Story editing by Ashleigh Graf. Copy editing by Paris Close. Photo selection by Ania Antecka.

This story originally appeared on Findbusinesses4sale and was produced and

distributed in partnership with Stacker Studio.