Home equity vs. credit cards: The smartest ways to handle post-holiday debt in 2025

Vitalii Stock // Shutterstock

Home equity vs. credit cards: The smartest ways to handle post-holiday debt in 2025

At the start of every new year, millions of Americans feel a massive holiday hangover, not just from their celebrations, but also from their suddenly inflated credit card balances. With the average American having credit card debt of over $6,000, holiday spending, inflation, and everyday rising costs only serve to exacerbate this value. Credit card interest rates have been above 20% since February 2023, meaning a small seasonal splurge can quickly become a prolonged and intensive burden.

For homeowners, however, there may be another answer. By leveraging the equity in your home, you can potentially consolidate your high-interest credit card debt into a lower-cost alternative. Splitero put together the numbers and built out this guide to compare credit card debt vs. equity financing agreements so that you can evaluate the best option for your finances.

Nothing is without risk, but having the chance to potentially save thousands of dollars in high-interest credit card debt can help you recover from your holiday overspending faster.

The credit card debt landscape in 2025

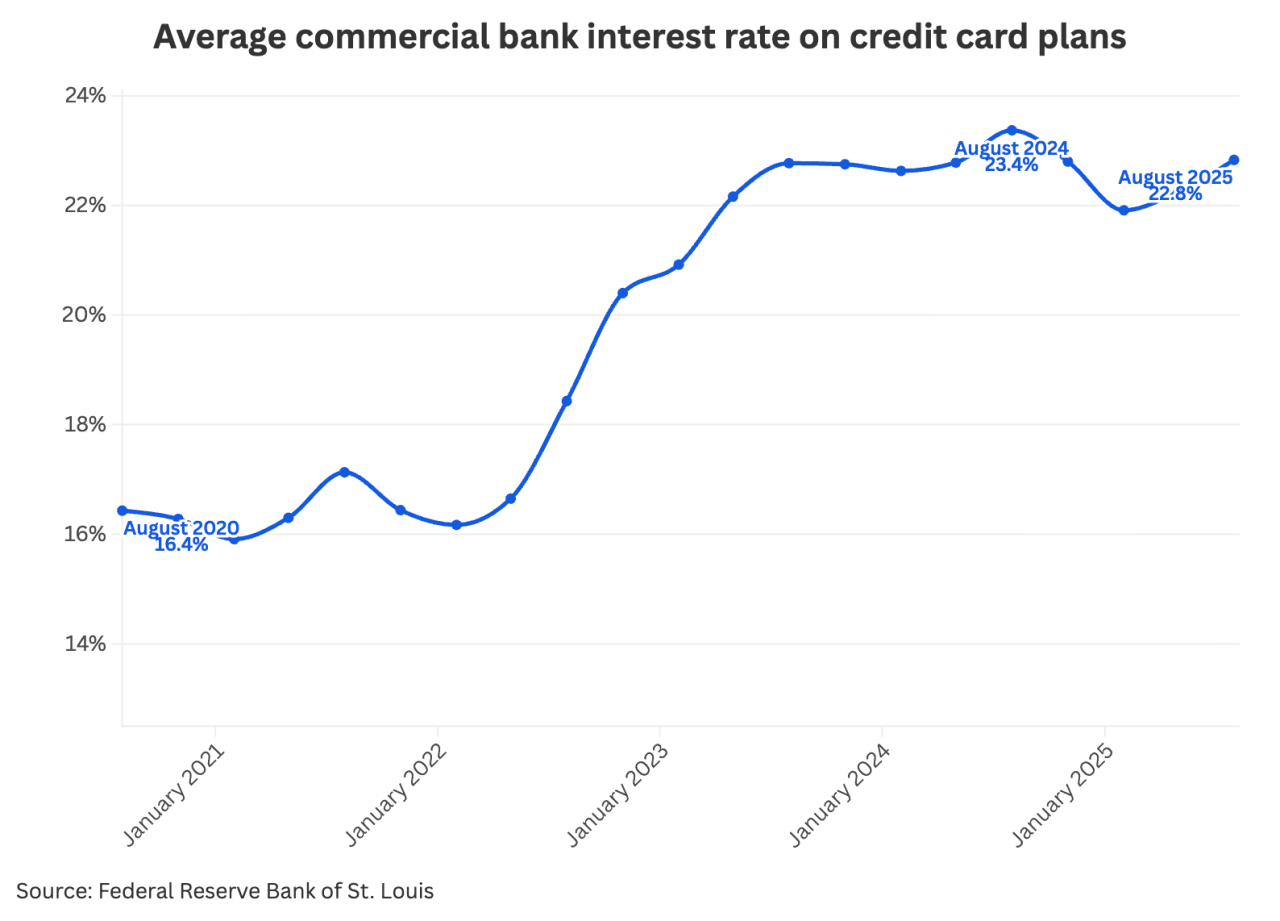

As mentioned, credit card balances for the average American are quite high. On a national basis, however, the latest data from the Federal Reserve System shows that revolving credit balances have grown beyond $1.3 trillion in July 2025. On top of this growing balance, the average APR across all credit cards has climbed to nearly 23% in recent years.

Splitero

This means that if you’re a holiday spender who chooses to put approximately $2,000 to $3,000 down on a card for gifts, travel, and dining, you may end up paying for these purchases well into the future. If only minimum payments were made on such a balance, it could take 5-10 years to pay off, based on the math at an assumed 20% APR.

The above scenario only takes one single credit card into consideration as well. If you have existing balances spread across multiple cards, it’s easy to see how things could quickly spiral out of control.

Homeowners: Why you have an advantage

Those who own a home sit in a unique position in this debt landscape. While a credit card balance is unsecured (not backed by collateral) and is a more expensive form of debt, homeownership builds a valuable asset that can be leveraged as collateral: equity. Home equity is simply the difference between what your home is worth minus the current balance of any loans or lines of credit secured by your home.

As of Q2 2025, homeowners collectively have over $35 trillion in home equity across the United States. This equity can be converted to cash through many different methods, though four stand out as the most prominent:

- Home equity loans: Under a home equity loan, you receive a lump sum loan with most often a fixed interest rate and repayment schedules

- Home equity line of credit: With a home equity line of credit, you receive a flexible revolving credit line that is secured by the value of equity in your home

- Home equity-sharing agreement: An equity-sharing agreement involves granting an investor the option to purchase a portion of the equity of your home in return for a lump sum of cash that requires no monthly payments. You may choose to repurchase the option at any time via a home sale, refinance, or cash settlement.

- Cash-out refinancing: With cash-out refinancing, you replace your mortgage with a larger one and pocket the difference

Borrowing against your home naturally adds some risk as your property becomes collateral if you don’t pay. On the flip side, it opens the door to much lower interest rates compared to credit cards due to the addition of security. As of October 2025, the national average home equity loan interest rate is 8.21% according to Bankrate, which is a far cry from the 20% or more that credit cards come with.

For homeowners faced with high-interest holiday debt, this difference presents a clear path to consolidating and paying off debt balances more affordably. The goal should always be to pay less in the long term than you are in the short term, so make sure to evaluate equity options against credit card options. In certain cases, depending on the debt balance in question, the longer timeline of most home equity options can result in more interest being paid, which is why you should crunch the numbers.

Comparing debt payoff scenarios: Credit card vs. home equity

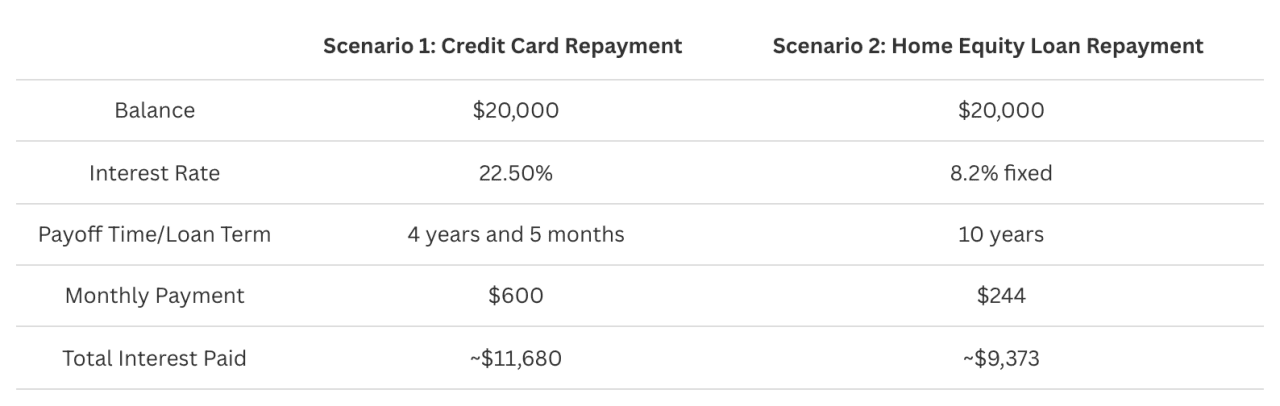

To illustrate the difference between these debt payoff strategies, let’s compare two scenarios. In the first, you’ll pay off a $20,000 credit card balance and the second, you ‘ll use a home equity loan for the same amount.

Splitero

Making the choice to shift your debt from a credit card to a home equity loan could help you cut your payments in half and save thousands in interest. For those with properties that have a fair amount of equity potential, home equity-sharing agreements can offer a lump sum up front with no monthly payments, which can be particularly helpful if your monthly cash flows are tight.

However, credit card debt is unsecured. If you default, your credit may suffer drastically, but you won’t necessarily lose your home. The stakes may be higher for home equity financing arrangements, but the trade-off is that the savings typically are as well.

Decision tree: Should you use home equity to pay off credit card debt?

Before immediately diving into an equity-based solution for your debt, it’s worth asking yourself a few questions to determine if this option makes sense for you. To that end, let’s construct a decision tree starting with key equations and then outlining potential yes or no paths from there:

1. Do you currently own your home and have at least 20% equity in it?

a. If yes, proceed.

b. If not, focus on unsecured debt consolidation via personal loans or balance transfers for now.

2. Are you carrying over $10,000 of high-interest credit card debt?

a. If yes, debt consolidation via home equity financing may yield savings. Consider proceeding.

b. If not, smaller balances can be better managed with budgeting when looking at potential interest owed on home equity options.

3. Can you afford another monthly payment?

a. If yes, maintaining your current debt may be possible.

b. If not, consider a home equity-sharing agreement as these come with no monthly payments.

4. Can you commit to not adding debt to your credit cards after payoff?

a. If yes, equity consolidation could break the one-time cycle.

b. If not, you are potentially risking doubling your debt by creating new credit card balances in addition to the home equity debt.

5. Are you comfortable using your home as collateral for debt?

a. If yes, proceed but exercise caution and ensure all payments are made on time.

b. If not, stick with unsecured debt financing options.

Be aware that to qualify for home equity terms that are favorable enough to justify debt consolidation, you will need to have decent credit. This is in addition to having adequate equity. If you don’t have one of these items, exploring alternatives may be the best choice. Otherwise, you may be saddled with a high interest rate that leaves you paying more than you would have otherwise.

Pros & cons of home equity vs. credit card debt consolidation

Regardless of the home equity financing option that you choose, there are several pros and cons compared to credit card debt. For instance, using home equity generally results in an interest rate that is nearly a third of the average credit card APR (7.7%-11.35% for home equity lines vs. an average 22.5% for credit card APRs). On top of this, home equity loans and lines of credit offer predictable payments, while equity-sharing agreements have no monthly payments.

Having one source of debt in a lump sum also simplifies your finances as opposed to having multiple debt streams across different credit cards. There may also be some tax benefits to using equity financing, as some interest may be deductible if funds are put towards home improvements, but you should consult a tax advisor.

Home equity financing isn’t without risk, though. Naturally, if you miss enough payments and go into default, foreclosure and the loss of your home may be on the horizon. Closing costs on home equity loans can also be around 1-5% depending on the loan value, according to Bankrate, which can be a significant burden. There is also the matter of spreading your debt out over 10 to 15 years, which may lower payments but increases total interest paid over time. If the long-term savings don’t add up to less than what you owe in interest on your credit cards, it may not be worth it.

Without having a financial plan or budget in place it’s easy to just generate more credit card debt back up which will double the burden and put you in the same exact position again down the road. When considering which home equity solution might be right for you, it’s essential to evaluate your finances carefully, including your spending habits, to determine the best way to handle your debt.

Next steps: Making a smart financial decision

If you’re a homeowner weighed down by credit card debt, especially during the holiday season, consider the following steps to evaluate your options:

- Assess your total debt: Add up all your credit card balances, interest rates, and minimum payments to see what you owe now and in the future

- Calculate your current equity: Subtract your remaining mortgage balance (and any other loans or lines of credit on your home) from the current market value of your home to get to this number

- Shop around for lenders: Compare different rates, fees, and equity options across a variety of banks, credit unions, third-party lenders, and other accredited sources

- Crunch the numbers: Use a loan calculator to model out savings as compared to paying off your credit card debt

- Take on new spending habits: Create a budget to improve your financial situation, and avoid falling into a cycle of debt in the future

- Seek out professional financial advice: Financial advisors and counselors are professionally trained to assist homeowners with navigating complex financial decisions through the use of tools and resources. These professionals can be an excellent resource to consult if you are unsure which home equity option is best for your needs.

It’s easy to quickly feel overwhelmed by the amount of debt you carry, especially if it’s coming from multiple sources. Don’t settle for paying sky-high interest rates if you have significant equity, don’t mind using your home as collateral, and can commit to better spending habits in the future. While the stakes are higher, the financial benefit might be worth the risk based on your personal circumstances.

Turn your holiday debt into a permanent financial reset

The holiday season should be a time of joy in your household as opposed to one of financial stress. However, with Americans shouldering an average $6,000-plus in credit card debt and interest rates climbing, it’s easy to lose the holiday spirit. For homeowners, accessing the power of equity in your home can provide a lifeline that lets you set up better spending habits while consolidating your debt into a single place.

By approaching debt payoff strategically and understanding your home equity options, you can alleviate your financial burdens. Get the fresh start you deserve by exploring the right home equity financing option for your needs.

This story was produced by Splitero and reviewed and distributed by Stacker.

![]()