What an LLC should look for in a business credit card

voronaman // Shutterstock

Business credit cards give your LLC dedicated spending power that’s separate from your personal finances. They simplify purchases, help you manage cash flow better, and build financial credibility with vendors and lenders.

These cards work for LLCs of all sizes. Startups can use them to cover early expenses while preserving cash. Small, established LLCs can track spending by category and streamline monthly accounting. Larger LLCs can provide company cards for employees, giving them spending power while maintaining control over expenses.

Ramp’s guide covers everything business owners need to know about LLC credit cards. You’ll learn about key benefits like building business credit, the application process, how to pick the right card, and get answers to common questions.

Benefits of business credit cards for LLCs

Business credit cards offer LLC owners tools—and credit limits—that personal cards can’t match. They include expense management, reporting, and spend control features designed specifically for running a company.

Some key benefits include:

- Streamlined accounting operations: Many business credit cards integrate directly with accounting software like QuickBooks and Xero. Pairing your card with expense management software gives you real-time visibility into spending and automates reconciliation, making account management and tax compliance significantly easier.

- Clear separation of business and personal expenses: Keeping your expenses separate helps protect your limited liability status. This makes tax preparation easier and helps protect your personal assets if your business faces financial issues or an audit.

- Employee expense management: Some business credit cards let you issue employee credit cards to team members who need purchasing power. These cards usually offer customizable spend limits and controls, helping you manage expenses more effectively.

- Rewards and perks: A dedicated credit card for your LLC gives you access to valuable rewards and perks that are tailored to business spending. Some cards offer elevated points or cashback on categories like travel, and some offer premium perks like airport lounge access.

- Building business credit history: Regularly using your card and paying your balance on time helps you build credit with major business credit bureaus like Dun & Bradstreet. A strong business credit profile can help you qualify for higher credit limits, larger loans, better vendor terms, and lower insurance rates later on.

These advantages help you run your LLC more efficiently and set it up for growth. By simplifying your financial operations, you can focus more of your time on growing revenue and less on administrative tasks.

What LLCs should look for in a business credit card

The best business credit card for your LLC depends on how you run your business, where you spend money, and what financial goals you have. A card that works perfectly for a retail business might not be right for a consulting firm or manufacturer. Taking a personalized approach helps you get the most value from your card.

Analyze your spending patterns

Start by looking at where you spend money. Review several months of bank statements to identify your biggest expense categories. If you spend heavily on travel, office supplies, telecommunications, or advertising, look for cards that give bonus rewards in those areas.

Project your cash flow needs

Next, think about your monthly business expenses and whether you expect any major purchases or investments over the upcoming year. A card with a higher credit limit will allow you to make larger purchases more frequently without tapping into your working capital. You might also consider 0% APR business credit cards if you need short-term financing flexibility for larger upfront expenses before revenue catches up. Additionally, some cards offer tiered rewards or bonuses when you hit a certain annual spending milestone.

Evaluate rewards and perks

Consider what type of rewards would benefit your LLC most. Cashback is simple and always useful. Travel rewards or airline miles can give you more value if your business requires frequent travel. Some cards also offer discounts or credits for services your business already uses, like software subscriptions or shipping.

Research fees and interest rates

Compare interest rates and fees based on your cash flow patterns. If your LLC often carries balances from month to month, prioritize cards with lower APRs. If you pay in full every month, look for business credit cards with no annual fees so you can maximize rewards without added costs.

Assess integrations and expense tracking features

Look for financial tools and features that could make your operations smoother. Modern business credit cards can integrate directly with accounting software, and some offer built-in expense management, receipt scanning, and customizable spend controls that can save you time and money.

To make your final choice, narrow your options to two to three cards that best match your spending profile. Compare their rewards potential based on your actual expenses, and consider any additional features that would benefit your operations.

How to apply for a business credit card as an LLC

Getting a business credit card for your LLC involves comparing card offerings, gathering business documentation, preparing personal information for guarantors, and completing the application process—typically taking 1-2 weeks from start to approval.

When you apply for a business credit card as an LLC, you’ll need to provide both business and personal information. Most card issuers require a personal guarantee from at least one member or manager, so they’ll likely check your personal credit, even if your LLC has been around for a while.

For standard business credit cards for LLC applications, follow these steps:

- Gather business documentation: Get your LLC’s legal name, employer identification number (EIN), business address, formation date, annual revenue, and estimated monthly spending

- Prepare personal information: Your guarantor will need to provide their Social Security number, personal income, and contact details. The primary applicant is usually an owner with significant equity or management authority.

- Research and select a card: Choose the card that best matches your LLC’s spending patterns and needs, using the criteria we discussed above

- Complete the application: You can typically apply online through the card issuer’s website, or call their business services line if you need help with a paper application

- Submit additional documentation if requested: Be ready to provide articles of organization, operating agreements, or business bank statements. Newer LLCs may face more scrutiny than established businesses.

Some business credit cards allow you to apply with an EIN only, but the process tends to be more restrictive. These cards typically require:

- Established credit history and a strong business credit score

- Significant annual revenue (often $1 million+) or substantial venture funding

- Business bank account with significant balances ($25,000–$100,000+)

- Longer operational history (typically 2+ years)

Troubleshooting common issues when applying for a card

Understand why you were denied

Getting denied for a business credit card can stall your LLC’s plans—but most rejections come down to a few fixable gaps in information or credit profile. Start by requesting the adverse action notice from the issuer. This document outlines the exact reason for your denial—often tied to insufficient business revenue, limited credit history, weak personal credit, or missing application details.

Double-check your documentation

Missing or incomplete documentation is a common—and often preventable—cause of delays or denials. Lenders need a clear, up-to-date view of your business, and any missing pieces can derail an otherwise strong credit card application. If you’re asked to submit additional documents, respond quickly and be precise. Common issues include outdated financials, missing proof of business address, or incomplete ownership information.

Explore options without a personal guarantee

In some cases, the issue isn’t paperwork—it’s the personal guarantee. If you’re not in a position to personally back the business credit card, focus on issuers that evaluate your LLC’s finances independently. These alternatives exist, but they often come with higher requirements—like strong business cash flow or large balances in your operating account.

Some corporate cards or charge cards may be more flexible. For example, business charge cards—where balances must be paid in full each month—may weigh business activity more heavily than personal credit. These products won’t fit every LLC, but they’re worth exploring if you’re building toward a guarantee-free future.

Improve your chances on the next application

Building toward stronger approval odds starts well before you fill out an application. Lenders look for signs that your business is established and financially reliable. That means building credit through vendor accounts, registering with credit bureaus, or even using a business credit builder loan. You’ll also want to match the card you apply for to your actual profile—secured cards or those designed for thin credit histories can be easier first steps.

It also helps to strengthen your existing financial relationships. Banks often favor current customers when evaluating new credit applications, and thorough documentation—showing revenue, cash flow, and account history—can make a difference. If personal credit is part of the review, improving your score there helps, too.

Put simply: The clearer your financial picture, the easier it is for issuers to approve your LLC for a business credit card.

Alternatives to business credit cards for LLCs

Business lines of credit are an alternative to credit cards if your LLC needs more substantial or flexible financing. Unlike credit cards, lines of credit typically give you access to larger amounts of capital—often with lower interest rates, especially if you have an established business with strong credit.

With a business line of credit, your LLC can draw funds as needed up to a set limit, similar to a credit card. However, lines of credit often have better terms for larger purchases or longer repayment periods. You only pay interest on the amount you borrow, not the entire credit line, making it cost-effective for occasional large expenses or seasonal cash flow needs.

Getting a line of credit as an LLC usually requires more documentation than a credit card application. Lenders often ask for business financial statements, tax returns, bank statements, and a detailed business plan. Many also require at least two years of operational history for unsecured lines of credit.

How does a new LLC get credit?

Brand new LLCs can often qualify for business credit cards within days of formation using two main approaches. Many new LLCs choose to leverage the owner’s personal credit history with a personal guarantee for faster approval, while others prefer building business credit independently to keep personal and business finances completely separate. Both paths are viable depending on your LLC’s needs and the owner’s preferences. New LLCs can establish credit through several approaches:

- Open business bank accounts first (foundation for all credit building)

- Choose between personal-backed cards (faster) or business-only options

- Register with business credit bureaus (essential for independent business credit)

- Establish vendor trade lines (builds credit history without personal involvement)

- Consider alternative options if traditional cards aren’t accessible

1. Establish business banking relationships

Opening dedicated business bank accounts is the foundational step for any new LLC seeking credit. Maintaining positive balances demonstrates financial stability to future lenders and creates the banking history that credit card issuers review during applications. Strong business banking relationships can sometimes substitute for personal credit requirements.

2. Choose your credit building approach

New LLCs have two main paths: using personal credit as backing with a personal guarantee (the fastest option), or building business credit independently without personal involvement. Some cards evaluate your business based on revenue and cash flow rather than personal credit, while traditional cards typically require personal guarantees.

3. Register with business credit bureaus

Registering your LLC with business credit bureaus like Dun & Bradstreet establishes your business credit file and enables future credit reporting. This step is especially crucial if you want to build credit without using personal credit, as it creates the infrastructure for tracking your business-only credit activity.

4. Build vendor trade relationships

Establishing relationships with vendors who offer net-30 payment terms creates trade lines that report to business credit bureaus independently of your personal credit. These arrangements demonstrate your business’s ability to manage debt and make timely payments without involving personal guarantees.

5. Consider alternative credit options

If traditional business credit cards aren’t accessible, explore secured business credit cards for guaranteed approval or corporate charge cards that focus on business cash flow rather than credit scores. These options can help build business credit while keeping personal and business finances separate.

What kind of business credit card can your LLC get based on your credit?

Not all LLCs are the same—and not all credit situations are either. Whether your company has strong business credit, a limited file, or is still relying on your personal credit, here’s what that means for your business credit card options.

If your LLC has good credit

LLCs with a strong credit profile—whether business credit, personal credit, or both—can typically qualify for unsecured business credit cards with higher limits, better rewards, and more features. These cards may offer cashback, points, or travel perks, and often include built-in tools for managing employee spending or integrating with accounting platforms.

Some issuers may still check your personal credit, especially if your LLC is under two years old. But if the numbers are solid, your options will be broad—including premium business cards, charge cards, and cards with large signup bonuses.

Best fits: Unsecured business credit cards, premium rewards cards, and charge cards with scalable limits.

If your LLC has fair credit

With fair credit—typically a score in the mid-600s—your LLC may still qualify for unsecured business cards, but the options will be more limited. Expect lower limits and fewer rewards, and prepare for a personal credit check if your business profile isn’t strong.

This is also where cards from your existing bank or cards designed for newer businesses can help. Some issuers consider your business bank account activity, not just your credit score.

Best fits: Entry-level business cards, no-annual-fee cards, and cards from banks where you have an existing relationship.

If your LLC has bad or no credit

If your LLC has no established credit—or if your personal score is under 600—you’re unlikely to qualify for traditional business credit cards. But that doesn’t mean you’re stuck. Many companies start by using secured business credit cards, which require a deposit but still help you build credit over time.

You can also look into corporate cards or charge cards that don’t require a personal guarantee. These often evaluate your cash flow or balance sheet instead of your credit score—but they may require significant revenue or reserves.

Best fits: Secured business credit cards, corporate or charge cards with no personal guarantee, and business credit builder programs.

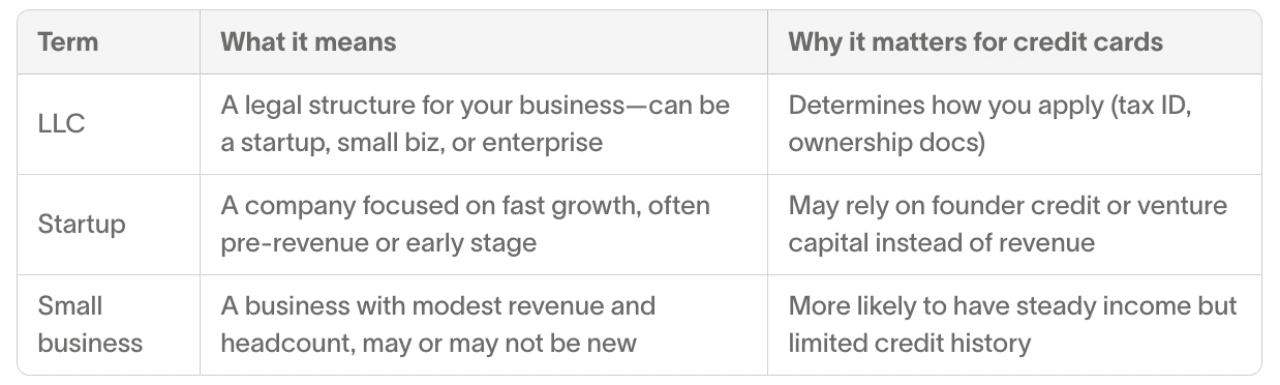

LLC vs. startup vs. small business: What’s the difference?

These terms get used interchangeably, but they don’t mean the same thing—and understanding the difference can help when you’re choosing the right card (or applying for one).

Ramp

So, your LLC could be a startup or a small business—or something in between. What matters for credit card applications is how long you’ve been operating, how much revenue you generate, what your credit profile looks like, and whether you’re personally guaranteeing the card.

Finally, choosing the best business credit card for your LLC: A decision framework

1. Understand how your LLC spends

Before comparing cards, start with your company’s financial reality. Your spending patterns are the biggest factor in determining which card delivers the most value.

- Review the last 3–6 months of business expenses

- Identify top categories (like advertising, travel, software)

- Estimate average monthly spend and any projected increases

- Note whether expenses are concentrated or spread across categories

This will help you determine whether to look for category-specific rewards or a flat-rate cashback card.

2. Evaluate how you manage cash flow

The right credit card should support—not strain—your company’s liquidity. Think about how your LLC uses credit today:

- Do you pay your balance in full or carry it month to month?

- Is financing flexibility more important than rewards?

- Do you need expense tracking and employee card controls?

If you carry a balance, a card with a low APR or built-in financing options may be worth a lower reward rate. If you pay in full, a charge card or rewards-focused option may make more sense.

3. Know your qualification profile

Even the best credit card won’t help if your business can’t qualify. Take stock of where your LLC stands:

- Personal and business credit scores

- Time in business and annual revenue

- Existing banking relationships

Your answers will narrow the field. For example, new LLCs or those with limited credit history should start with no-annual-fee business cards, secured credit cards, or options from your current bank. If your LLC has strong revenue or an established credit profile, you may qualify for premium business cards with higher limits and more rewards.

4. Match card features to your operational needs

Once you’ve narrowed down the options, compare features based on what matters most to your business:

- Rewards structure: Flat-rate vs. category-based

- Fees: Annual fees, foreign transaction fees, late payment penalties

- Spend controls: Customizable employee limits, card issuance

- Reporting tools: Integration with accounting software or spend platforms

High-growth LLCs often benefit from cards that offer scalable limits, expense visibility, and flexible card controls. If your business operates internationally, look for cards with no foreign transaction fees and global acceptance.

What the best card actually looks like

The best business credit card for your LLC isn’t a universal pick—it’s the one that aligns with four key factors:

- Your real-world spending habits

- Your approach to cash flow and credit

- Your current qualification profile

- Your operational priorities and tooling

Get those right, and the rest—rewards, limits, even perks—will fall into place.

This story was produced by Ramp and reviewed and distributed by Stacker.

![]()