How American borrowing showed resilience amid initial 2022 interest rate hikes

Chen Mengtong/China News Service // Getty Images

How American borrowing showed resilience amid initial 2022 interest rate hikes

Federal Reserve Chair Jerome Powell attends a news conference.

As the Fed raised interest rates last summer, the increased cost of borrowing didn’t dampen the popularity of taking out new personal loans, which saw steady increases in the U.S.

Experian examined the Federal Reserve’s federal funds target rate and its own personal loan origination data to see how rising interest rates are impacting Americans’ decisions to take out personal loans.

A personal loan is a type of credit that’s disbursed in one lump sum by a bank or other entity and repaid over time in fixed monthly payments. Personal loans don’t typically require collateral, like with a car loan or mortgage. People take out personal loans for a variety of reasons, including consolidating debt that carries varying interest rates, paying medical bills, or making home improvements.

These loans are a popular vehicle for everyday Americans to borrow money—4 in 5 surveyed consumers said they’re aware of personal loans, according to a OnePoll survey of 2,000 Americans conducted on behalf of Forbes in the first quarter (Q1) of 2022. Three in 5 respondents said they have used a personal loan in the past.

Personal loans tend to have fixed interest rates, but the interest rates on newly issued personal loans can fluctuate with economic conditions and other factors. The Federal Reserve’s board is charged with keeping both inflation and unemployment under control, and its primary method of achieving those goals is setting the federal funds target rate. Sometimes simply referred to as the federal funds rate, it is the range of interest rates banks can charge one another to borrow money to meet the minimum cash-on-hand requirements that ensure their institutions are solvent.

Banks set their interest rates by adding percentage points to the federal funds rate to cover their costs of operations, account for the risk inherent in making loans, and generate profit. So when the Fed raises its rate, banks raise theirs in turn. When interest rates rise, it becomes more expensive to borrow money and, historically, consumers are inclined to borrow less.

The Federal Reserve began hiking interest rates in early 2022, with the first hike announced in March, which was followed by six additional increases by the end of the year. The number of personal loans taken out by consumers in the U.S. grew 87% from Q2 2019 to Q2 2022. In Q2 2022, the average interest rate on a two-year personal loan was 8.73%, according to data from the Federal Reserve. That rate was still lower than the rate for a two-year personal loan in 2019, which was 10.3% on average.

And while the federal funds rate is consistent across every state in the U.S., there were regional differences in how Americans took out loans as interest rates rose. Southern states recorded the highest growth in personal loan debt, both in the number of loans taken out and their dollar amounts.

![]()

Experian

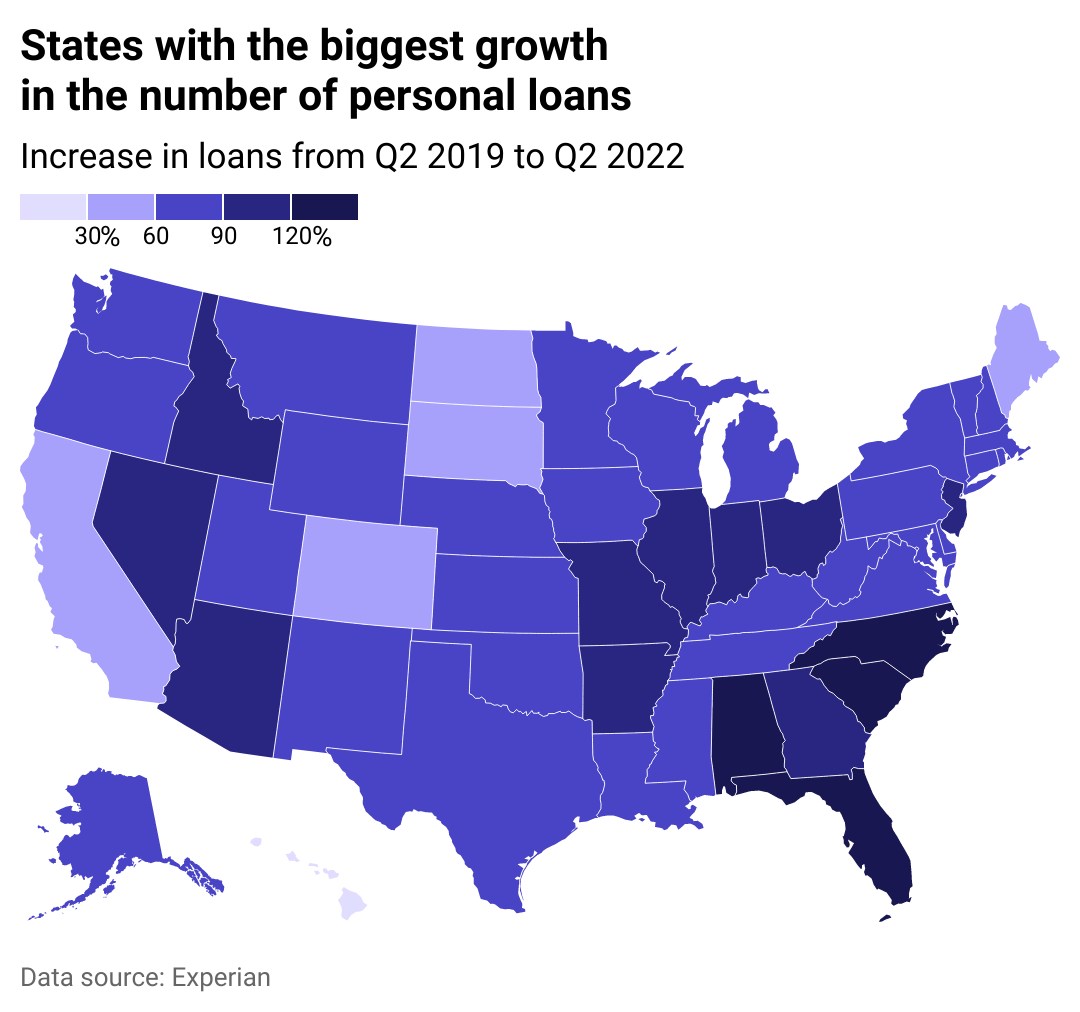

More loans are being issued to consumers in the South

A heat map showing which states are taking out more personal loans.

If the Federal Reserve’s ultimate goal to combat inflation is to slow borrowing activity, the initial three interest rate hikes in 2022 had perhaps the least effect in North Carolina, South Carolina, Florida, and Alabama. In these Southern states, consumers took out twice as many personal loans in early 2022 compared to early 2019.

The number of personal loans issued to Americans in every state grew from Q1 2019 to Q2 2022. The number of loans grew slowest from 2019 to 2022 in Hawaii, Maine, the Dakotas, California, Colorado, and Vermont.

Experian

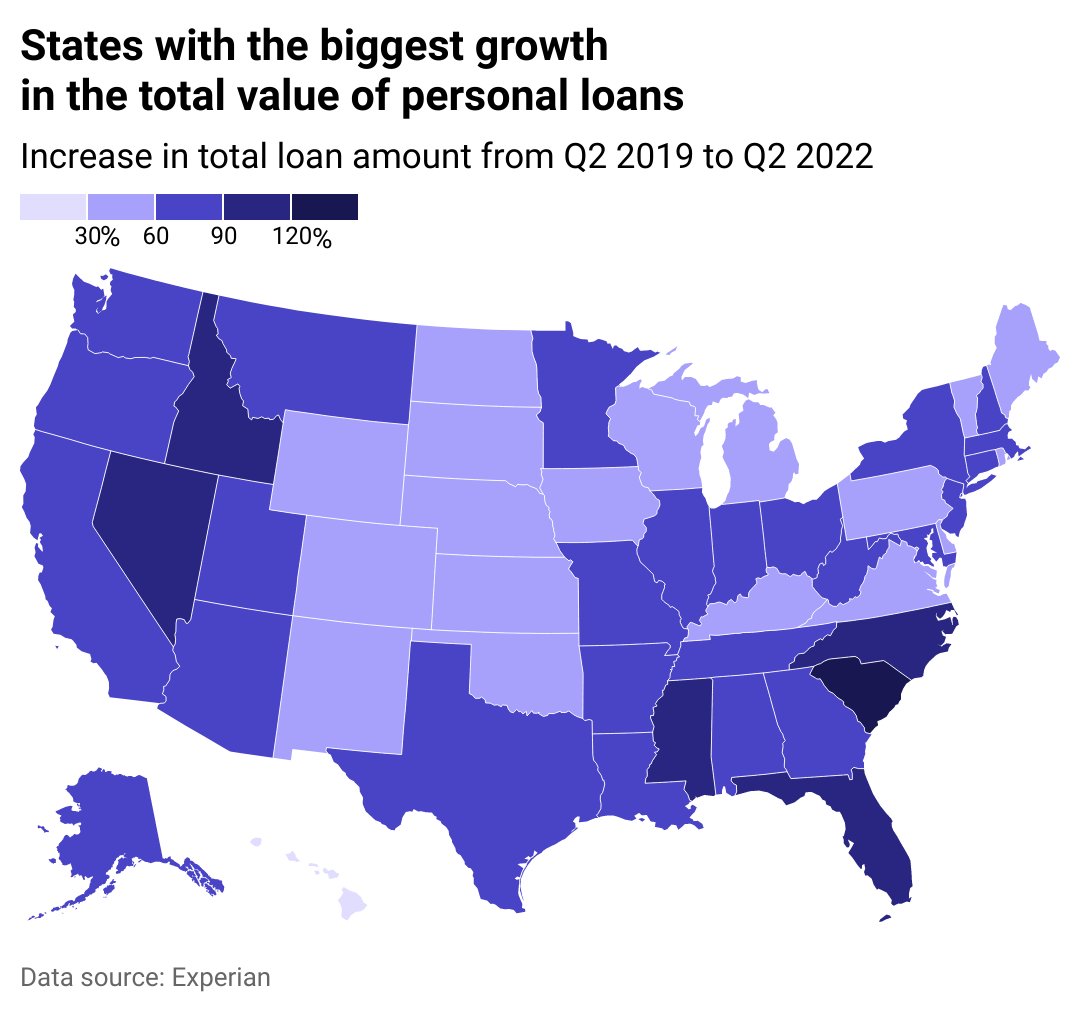

Southerners are also taking out higher loan amounts

A heat map showing which states taking out more money in personal loans.

The parts of the U.S. that saw the total value of loans taken out by consumers grow between Q2 2019 and Q2 2022 were similar to where loan volume has increased the most.

Loan volumes more than doubled over that period in South Carolina, Mississippi, and North Carolina, according to Experian data. States that experienced an influx of new residents over the pandemic—including Texas, Arizona, Georgia, Nevada, Florida, and Idaho—also saw above-average personal loan value growth.

Experian

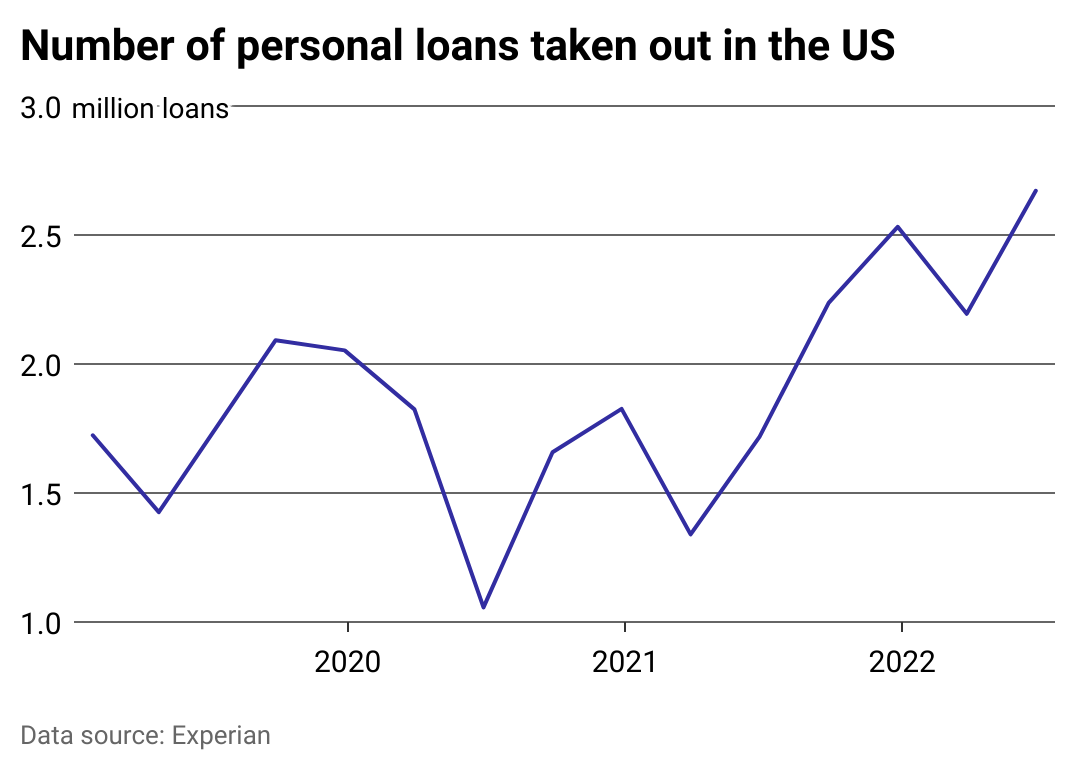

More consumers are borrowing personal loans

A line chart showing the number of personal loans taken out in the U.S.

Despite rising interest rates, more Americans took out personal loans between Q2 2021 and Q2 2022 than during the same period in 2020 or 2019. Seasonally, people tend to take out fewer loans in the first quarter of the year, with the number increasing into the fourth quarter.

Experian

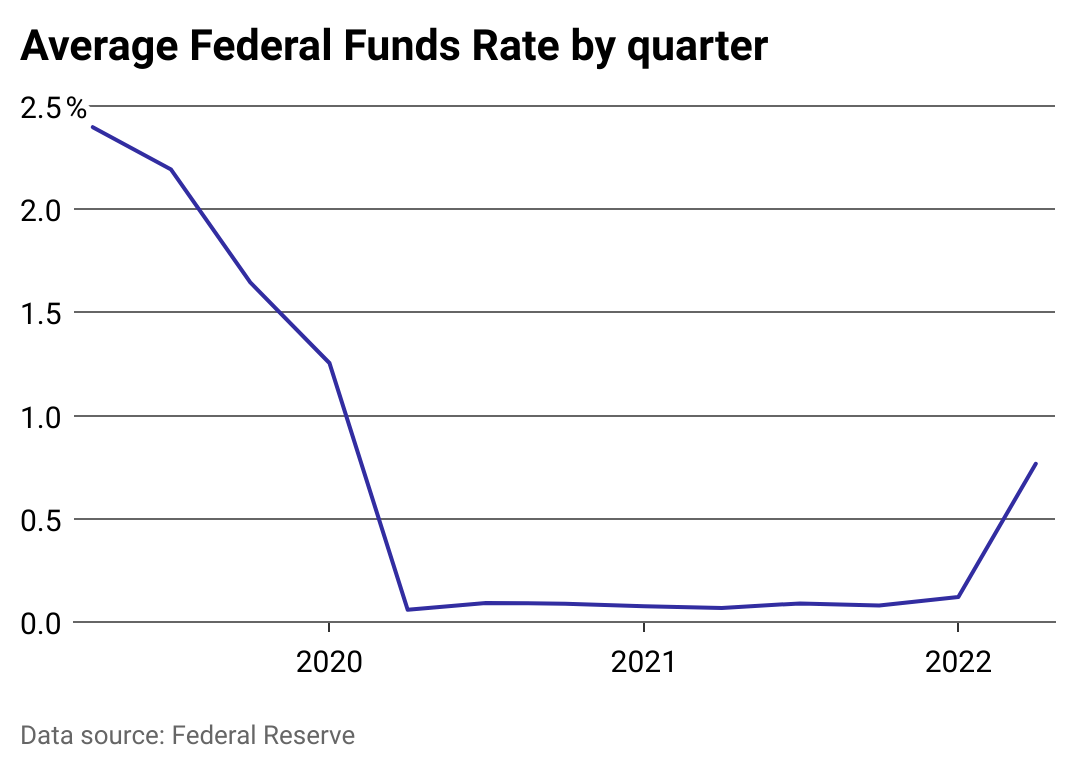

Interest rates are expected to keep climbing

A line chart showing the average Federal Reserve interest rate by quarter.

The Federal Reserve acted quickly after the COVID-19 pandemic’s emergence in 2020, anticipating the economy would be stressed by increased unemployment and other factors. It lowered the federal funds rate to nearly 0% from the already historically low rates that had followed the Great Recession. Its board of governors has since hiked rates repeatedly, issuing seven total increases in 2022; the potential effects of increases after Q2 2022 aren’t captured by this data.

Economists have voiced mixed opinions as to whether the rate hikes announced by the Fed through Dec.14, 2022 will be sufficient to tamp down inflation, which reached 40-year highs in 2022. They’re also divided as to how long it will take to see the economy feel the effects of the Fed’s actions this year.

This story originally appeared on Experian and was produced and

distributed in partnership with Stacker Studio.