Are homeowners using their home equity to pay for home improvements? Do they even know they can?

Zivica Kerkez // Shutterstock

Are homeowners using their home equity to pay for home improvements? Do they even know they can?

Two people in charge of overseeing a home improvement where one woman is leaning on a table with blueprints and noting with an instrument and the other is a man hammering nails on a wall.

Almost one-half of all mortgaged residential property owners were considered equity rich at the end of 2023, according to the U.S. Home Equity & Underwater Report from ATTOM, a top collector of property and real estate data. That means they had built up at least 50% equity in their homes, putting them in a good position to utilize it for home improvements.

But in an environment of high interest rates, people with lower interest rate mortgages may be unwilling to change the terms on their current mortgage to access that equity. There are other options available, but how aware of these options is today’s homeowner?

To find out, Rocket Loans surveyed 1,000 homeowners on different methods of financing home improvements, including using a home equity loan.

79% Of Homeowners Failed To Define A Home Equity Loan

A home equity loan allows a homeowner to convert existing equity in their home into cash without refinancing their primary mortgage. It’s a second mortgage, which means an additional payment on top of the primary mortgage, and potentially meaning the rate is slightly higher than if they refinanced their existing mortgage.

When asked to choose the correct definition of this type of loan, 79% of homeowners got it wrong.

A little over one-fifth (20.8%) thought it increased their primary mortgage, while also keeping the same interest rate. And, though 58.2% did know that it’s a second mortgage that allows a homeowner to borrow equity, they thought it could only be done through a line of credit.

What they’re thinking of is a home equity line of credit (HELOC). These loans provide access to funds much like a credit card. The borrower can draw from a revolving line of credit – with a credit limit – and even put funds back in through repayment during the draw period. A home equity loan delivers the funds through a lump sum payment with no draw period – just a repayment period that starts after closing.

This lack of home equity loan knowledge may be one reason the majority of homeowners (71.7%) have never gotten this type of loan. It’s believed these loans should be more popular than other financing options because, in a higher interest rate environment, loans secured by a home will receive some of the lowest interest rates borrowers can get for any loan option. So what are they using instead?

Almost 21% Of Homeowners Don’t Know How Much Equity They Have

The amount of equity someone can borrow is tied to how much equity they have in their home. Unfortunately, about one-fifth of owners don’t even know how much they have. Of all the respondents:

- 4.7% had less than $10,000

- 16.7% had $10,000 – $50,000

- 17.7% had $50,000 – $90,000

- 15.9% had $90,000 – $150,000

- 8.8% had $150,000 – $200,000

- 15.5% had over $200,000

- 20.7% don’t know

Those who don’t know how much equity they have, an online estimator can provide a starting point for home value. Once they have that number, they can subtract what they owe and that will give them a ballpark amount of equity in the home. Lenders will only allow borrowers to take out a percentage of their equity and may require a minimum loan amount.

For projects worth less than that amount, a personal loan can be a good option. Because they’re unsecured, these loans would generally have higher rates than home equity loans, but lower rates than credit cards.

Home equity loans and personal loans can be good options for costlier home improvements, but how many homeowners are actually using them? And if they’re not using these methods of financing, how are projects being paid for?

![]()

Rocket Loans

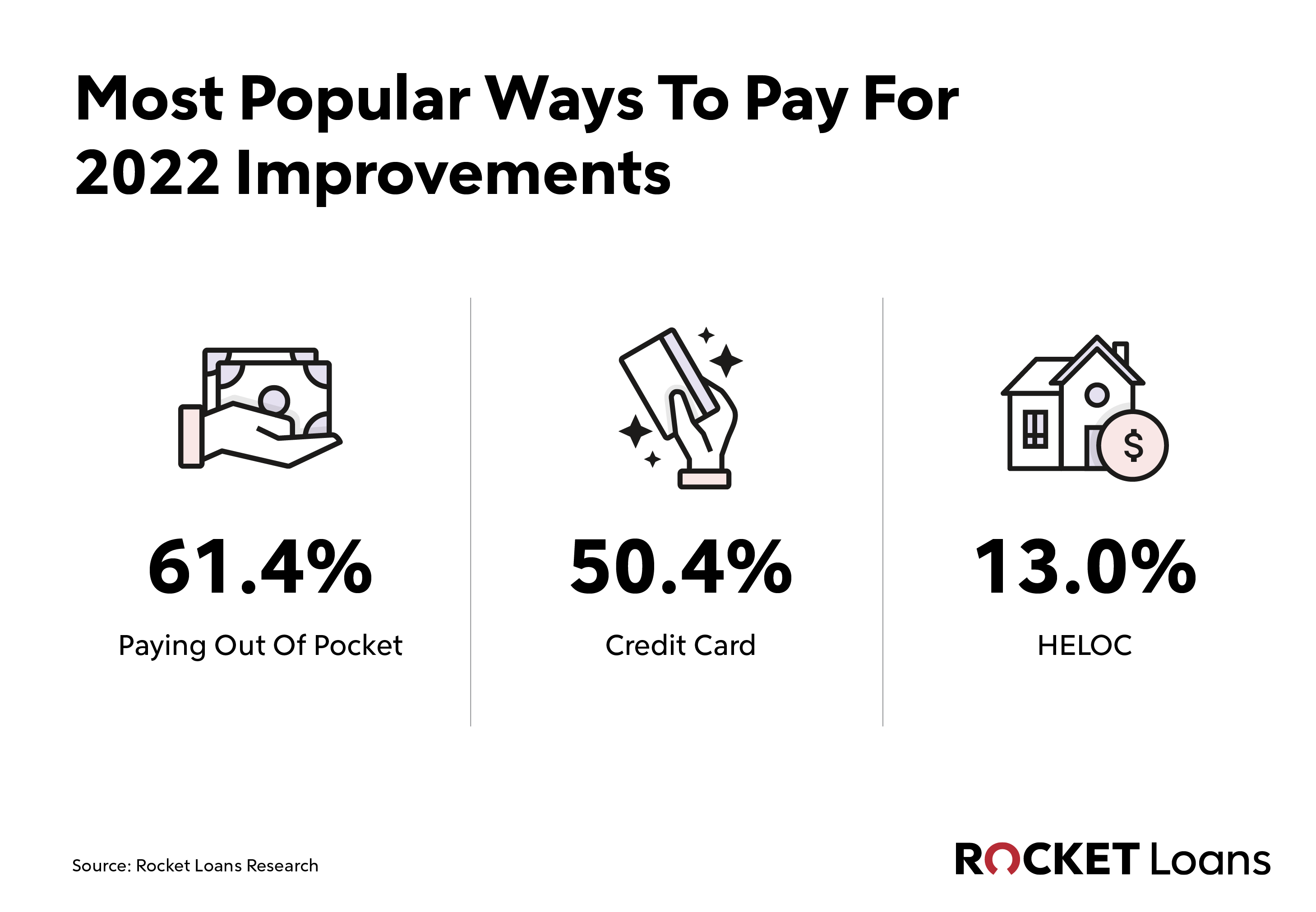

Cash And Credit Card Are The Most Popular Ways To Pay For Home Improvements

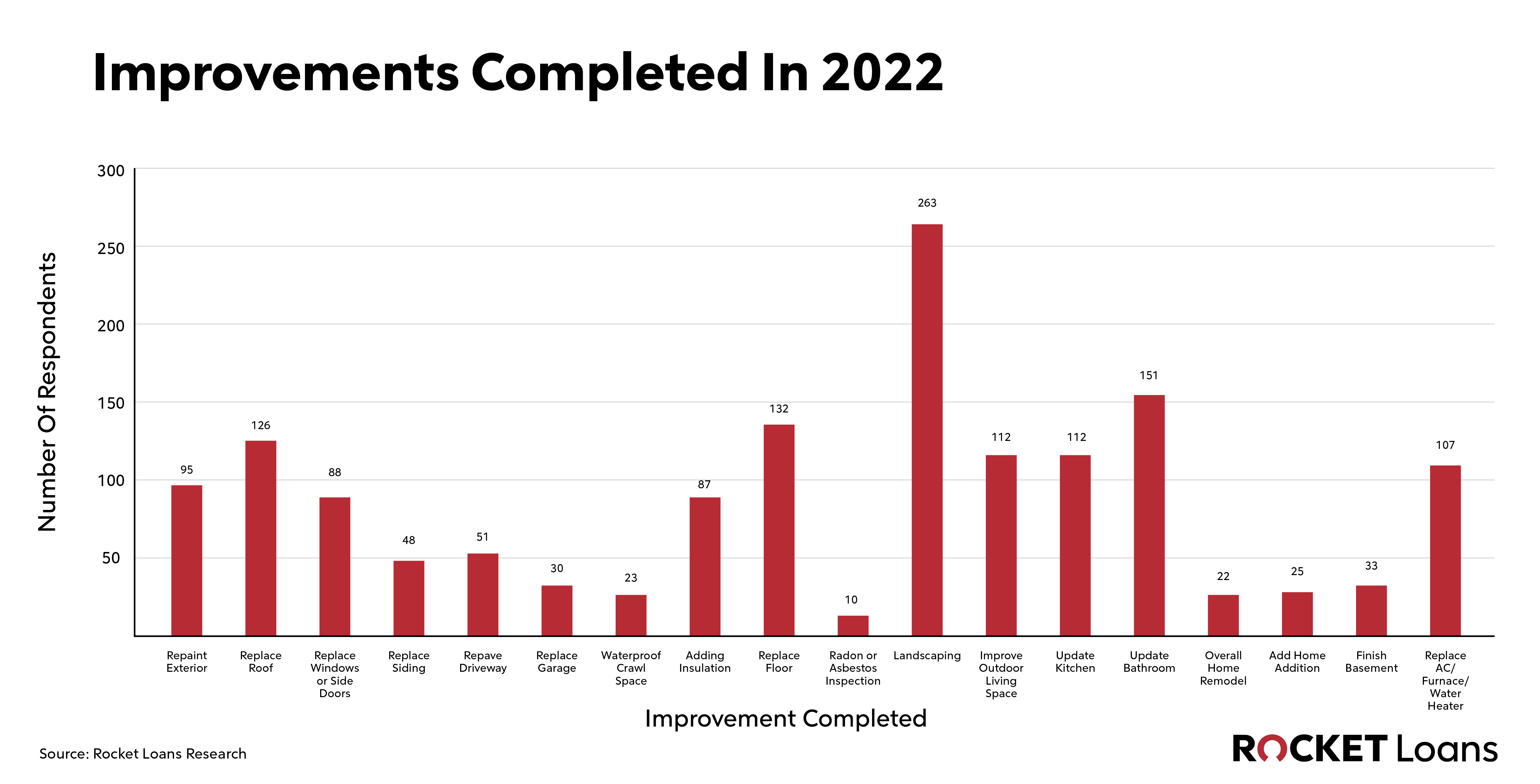

Chart showing Improvements completed in 2022.

In 2022, 61.9% of homeowners completed at least one of the 18 home improvement projects listed below.

According to the Rocket Loans survey, this is how they financed at least one of these projects:

- 61.4% paid for some or all of their project costs out-of-pocket.

- 50.4% paid for some or all of their project’s costs with a credit card.

- Only 13% paid for some or all of their project costs with a HELOC.

- Only 8% paid for some or all of their project costs with a home equity loan.

Rocket Loans

Payment methods didn’t include personal loan

Infographic showing Most Popular Ways to pay for 2022 Improvements

While other methods of payment included contractor financing, investments, insurance and refinancing, no one claimed to have used a personal loan.

This is somewhat surprising because, outside of financing through home equity, personal loans can be attractive based on having much lower rates than credit cards. The payment is also fixed, where a credit card rate can change every month. Finally, some like that it’s not tied into the home. So while it may be harder to qualify, the home isn’t at risk.

Rocket Loans

Paying For Home Improvements In 2024

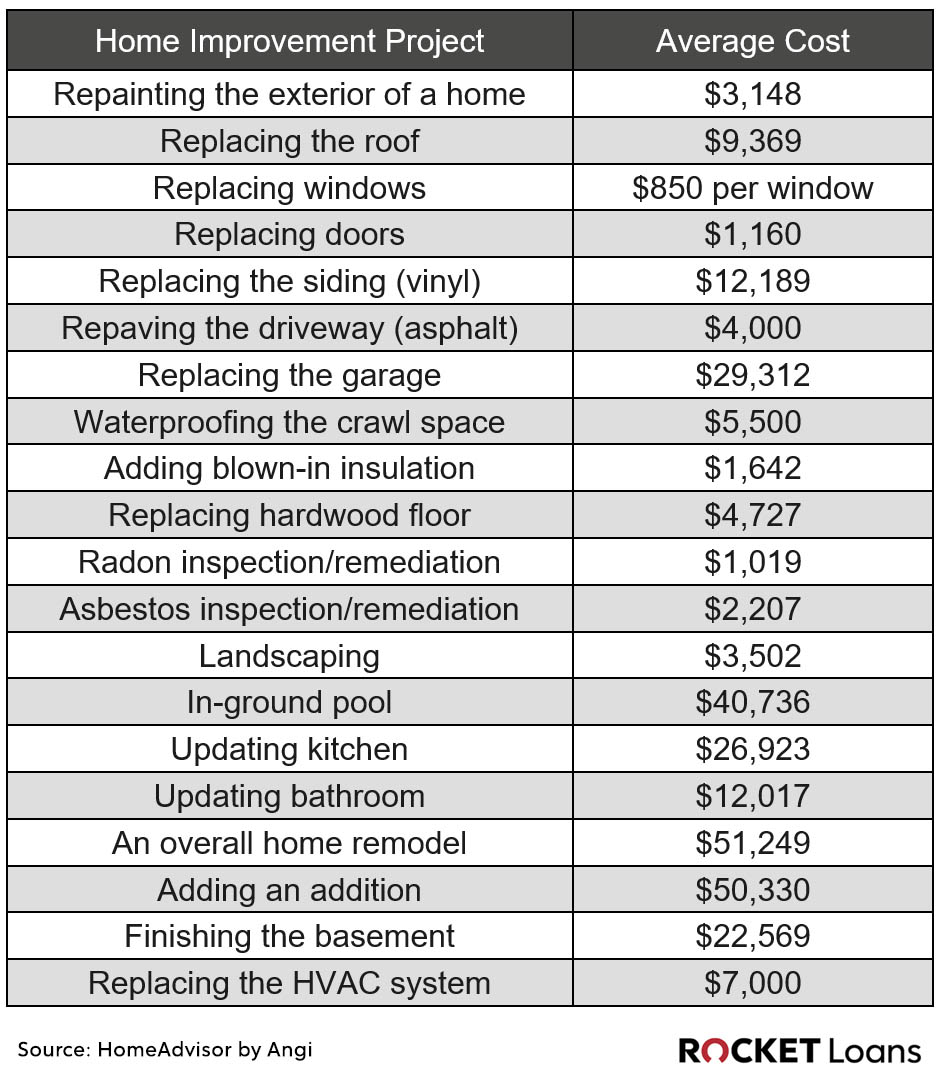

A table showing different home improvement project categories and their average cost.

The table above represents national averages for the cost of certain projects, according to the latest data available from HomeAdvisor by Angi. Note that some of these costs will vary based on the materials used and the cost of labor.

Bottom Line: Homeowners Could Be Overpaying For Financing

Given the amount of equity available to homeowners at this time, they’re likely missing opportunities to use the money invested in their home to improve its value through various projects. A home equity loan provides the opportunity to capitalize on this without having to refinance their primary mortgage. However, homeowners do need to have enough equity to borrow and lenders have minimum loan amounts.

For smaller projects, personal loans may be utilized. These interest rates are higher than those for loans secured by a home, but they’re significantly lower than typical credit card interest rates, occupying an important middle ground in terms of financing.

Methodology

To understand more about homeowners’ knowledge of home equity loans, their past home improvement projects and how they financed them, Rocket Loans surveyed 1,000 American homeowners 25 years and older with a mortgage. Homeowners were asked about their knowledge on home equity loans as well as how much home equity they have tied up in their property. They were also asked about home improvement projects they have completed already in the past year, what plans they have for the next 2 years and how they feel about these different projects. This survey was conducted March 13, 2023. The 2024 home improvement costs listed in this article are sourced from HomeAdvisor by Angi and were reviewed on April 24, 2024.

This story was produced by Rocket Loans and reviewed and distributed by Stacker Media.