Survey: How drivers are managing auto insurance premium increases

BLACKWHITEPAILYN // Shutterstock

Survey: How drivers are managing auto insurance premium increases

Car insurance bills are seen with a red toy car, coins and a calculator on top of it.

If you’re behind the wheel in 2024, you already know how expensive driving has gotten. Not just because of the monthly payment and the price of gas, but also because of the rising cost to insure your vehicle in the event of an accident.

According to consumer price index (CPI) data, motor vehicle insurance costs represent nearly 3% of a typical consumer’s budget. And while premiums were flat during the pandemic, when Americans sharply curtailed their driving, the cost of auto insurance premiums has gone in no direction but up ever since.

Experian surveyed 1,018 consumers about their auto insurance policies. The survey was conducted on May 13, 2024. The sample was collected using a third-party company and was not from Experian’s consumer credit database.

![]()

Experian

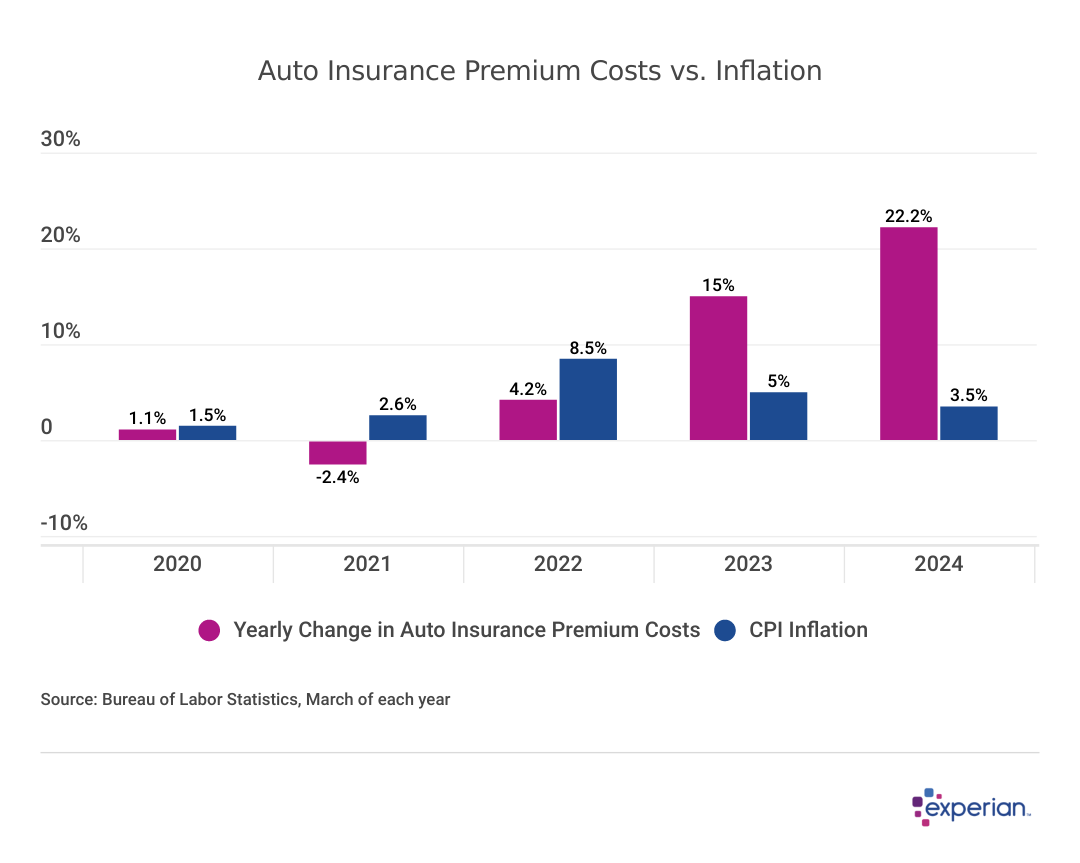

Insurance Premiums Continue to Increase Despite Lower Inflation

Graph showing results for “Auto Insurance Premium Costs vs. Inflation”.

But despite the 43% cumulative increase in insurance premiums since 2020, at least some drivers appear unmotivated to lower their costs, according to a May 2024 Experian survey. Let’s take a look at what drivers are—and aren’t—willing to do to get auto insurance costs under control.

Experian

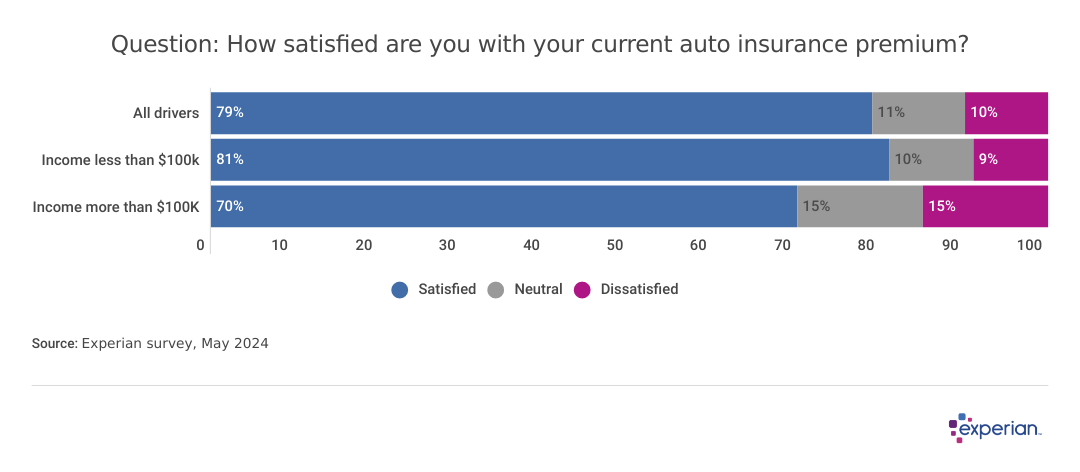

Higher-income Households More Dissatisfied With Cost of Auto Coverage

Graph showing results to the question: “How satisfied are you with your current auto insurance premium?”

It sounds a bit counterintuitive, but drivers who make more money are generally less content with their auto insurance costs, according to our survey. Among drivers with an annual household income above $100,000, 15% say they’re dissatisfied with their premiums, versus 9% dissatisfaction among drivers who make less.

One possible explanation: Those with higher incomes are more likely to drive more expensive vehicles with higher associated repair costs—particularly electric vehicles, which are more popular among households with higher incomes.

Experian

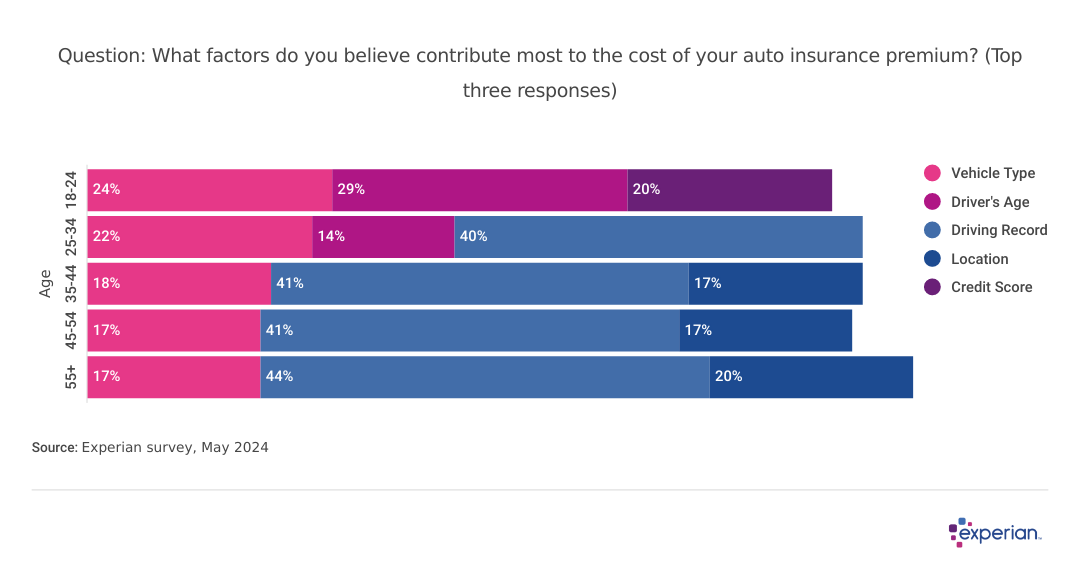

Most Drivers Tick Driving Record, Type of Vehicle as Having Greatest Impact on Costs

Graph showing results to the question: “What factors do you believe contribute most to the cost of your auto insurance premium? (Top three responses)”.

Overall, most drivers surveyed credited (or blamed) their driving record, the type of vehicle they drive and where they live as having the greatest impact on their auto premiums. The one exception was drivers ages 18 to 24, who cite a major factor besides vehicle type—their age.

They’re not wrong. Their lack of driving experience means younger drivers are generally more costly to insure. Vehicle type, model and age all factor into the premium quote you’ll receive from an insurer. Also, as credit scores tend to be lower for younger drivers, this may also be a bigger factor for younger drivers in states where credit-based insurance scores are used.

Experian

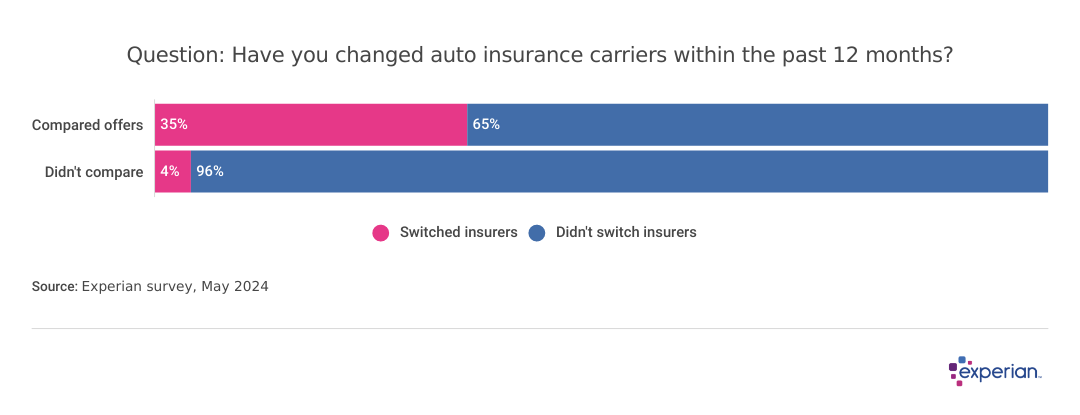

Drivers Who Shop for Lower Auto Insurance Premiums Often Switch

Graph showing results to the question: “Have you changed auto insurance carriers within the past 12 months?”

When asked if they have recently compared premium rates across insurers, about half said that they’ve looked for alternative coverage in the past year, while the other half didn’t. Among those who did some price and coverage comparison shopping, however, more than 1 in 3 drivers ended up switching insurers.

Experian

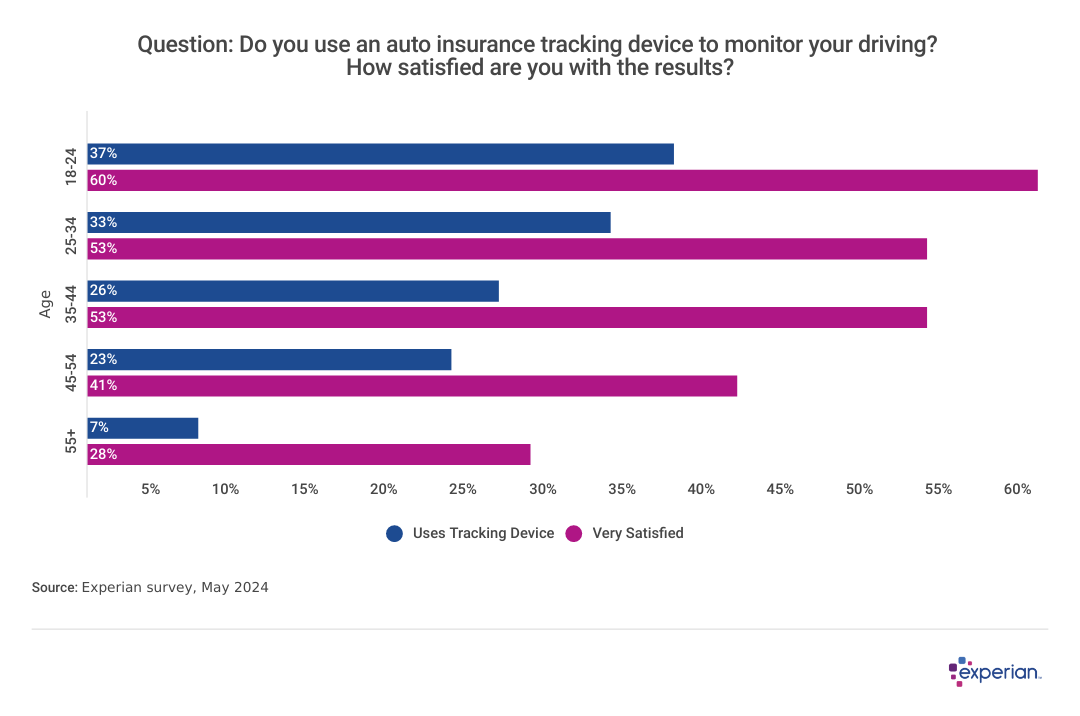

Drivers Mostly OK With Devices That Track Driving for Insurance

Graph showing results to the question: “Do you use an auto insurance tracking device to monitor your driving? How satisfied are you with the results?”.

Although some drivers are averse to having their driving tracked, most surveyed drivers said they’re at least content with having their insurance company monitor their driving, either by their smartphone or with equipment installed in a vehicle’s dashboard.

The enthusiasm, or lack thereof, for monitored driving appears to be age-dependent. Older survey respondents indicated they aren’t as quick to embrace the newish technology as younger drivers. This may be due to the fact that younger drivers are more incentivized to demonstrate their safe driving habits to lower their premium when they renew coverage. It could also be that younger drivers are more eager or willing to accept technology in their driving lives than older U.S. drivers clinging to more romantic notions of the open road.

Other Popular Ways to Lower Insurance Premiums

Even if shopping for another insurer or having your driving electronically tracked aren’t for you at the moment, there are still other ways to reduce your auto premium costs. The most popular ways to save among drivers we surveyed were:

- Bundle multiple types of insurance with one provider (24% of drivers said they did in the past year)

- Reduce collision coverage on older vehicles they own (15%)

- Increase the deductible in the event of a claim (13%)

- Sell one or more of the vehicles they own (9%)

In most states, improving your credit can be another way to bring down insurance costs. Credit-based insurance scores differ from the scores that lenders use but are based on many of the same factors, including payment history, credit utilization and recent inquiries.

This story was produced by Experian and reviewed and distributed by Stacker Media.