In-depth comparison: PPOs vs EPOs

Pranithan Chorruangsak // Shutterstock

In-depth comparison: PPOs vs EPOs

Female healthcare professional guiding patient in filling up insurance forms.

There is no one-size-fits-all solution to health insurance. Employers can offer a variety of healthcare plans to their employees, and two popular options are Preferred Provider Organizations, or PPOs, and Exclusive Provider Organizations, or EPOs.

Both plan types offer unique benefits but also have some key differences that employees need to be aware of before they choose which type of healthcare plan to enroll in.

PPO: This plan offers high flexibility, allowing visits to any doctor or specialist without referrals, including out-of-network providers, at a higher cost.

EPO: Requires using in-network providers for non-emergency care, leading to lower premiums but no coverage for out-of-network services.

Key Differences: PPOs are best for those needing flexibility and frequent specialist visits; EPOs are suitable for those with infrequent health care needs and lower costs.

Thatch takes a closer look at how PPOs and EPOs work.

What Is a PPO?

A PPO plan offers a higher degree of flexibility when it comes to choosing health care providers. With a PPO, you can generally visit any doctor or specialist, in-network or out-of-network, without a referral. PPO plans typically do not require selecting a primary care physician, which may be preferable for those who don’t currently have a specific doctor they want to see. For example, let’s say an individual has a PPO plan and needs to see a specialist. They can choose any specialist they prefer and schedule an appointment. The services that the specialist provides will typically be covered by the insurance plan—even if they are not in the plan’s network (but most likely at a higher cost). While the cost for that out-of-network specialist may be higher than for in-network providers, the individual still has the option to receive care from them.

PPOs are often a good option when employees switch health care coverage because their new network may not provide them with access to the same physicians they already have relationships with. If someone receives ongoing care, they may appreciate the stability a PPO can offer—even if they need to pay more to see an out-of-network provider.

What Is an EPO?

An EPO plan operates in a more tightly controlled way than a PPO. Under an EPO, a person must seek medical services from providers within the plan’s network unless it’s a true emergency. EPOs typically do not cover any out-of-network services (again—except emergency services). The individual may be responsible for the full cost if they choose to receive care outside of the network for non-emergency situations.

However, for those who don’t anticipate the need to visit specialists who might be out of network, or whose health care needs are more infrequent, EPOs often have much lower monthly premiums than PPOs. For instance, let’s say a person visits the doctor once or twice a year, and if they need to visit a specialist, their doctor refers them. In this case, an EPO plan might be preferable as it’ll be much less expensive month to month, especially if they’re visiting an in-network specialist.

EPOs may be a solid choice for healthy employees—particularly young ones—who only go to the doctor on occasion or who are worried about running into emergency health care costs one day.

Key Network Distinctions

Here’s a quick recap of the major distinctions when it comes to PPOs vs. EPOs.

- PPO Networks: One of the key advantages of PPOs is their flexibility. You have the option to visit both in-network and out-of-network providers. This flexibility is particularly useful if you travel frequently or prefer seeing specialists who may not be in-network. However, keep in mind that choosing out-of-network care usually involves more paperwork and higher costs.

- EPO Networks: EPOs require you to stick to in-network providers for any non-emergency care. While this might seem restrictive, it often translates to lower premiums and reduced out-of-pocket expenses compared to PPOs. EPO networks are typically narrower, and care outside of this network may often not be covered, except potentially in emergencies.

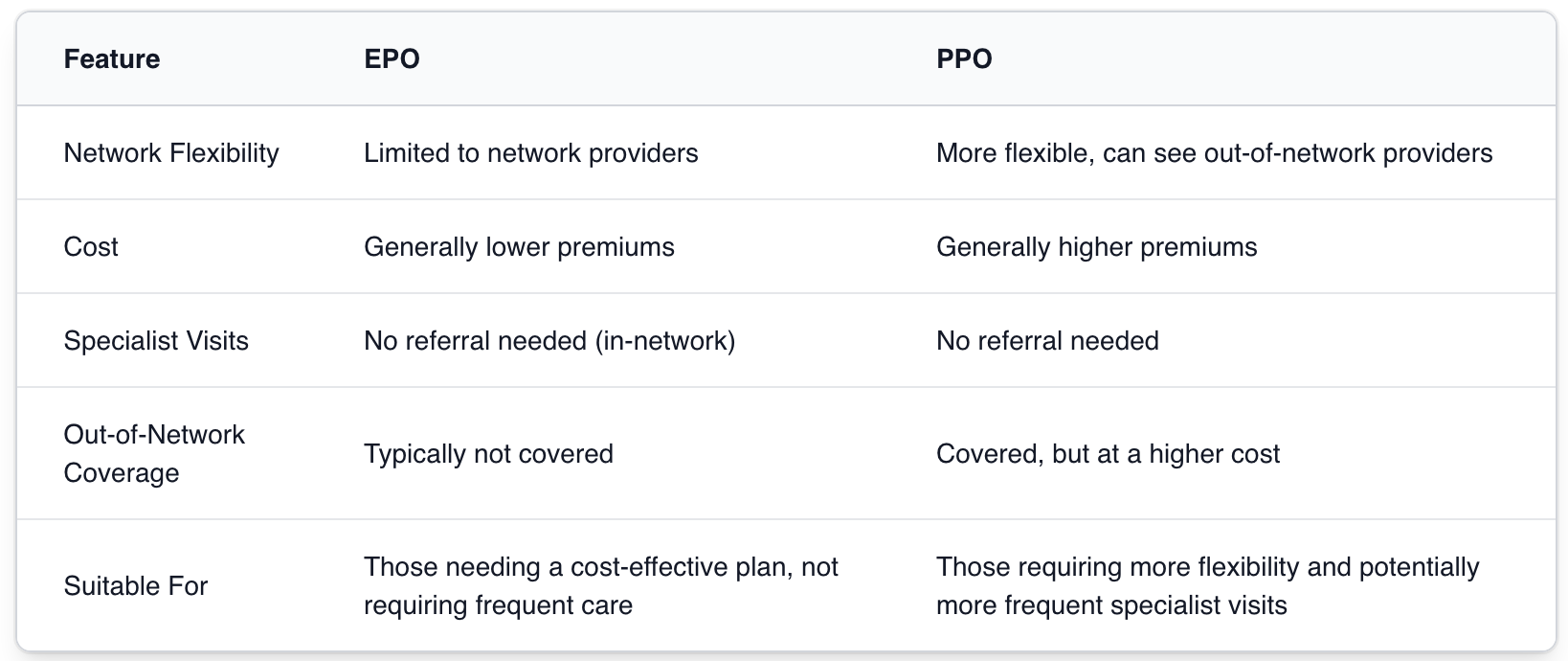

To summarize for ready reference:

![]()

Thatch

Tiered Networks Offer Lower Costs With Preferred Providers

Table showing differences between EPOs and PPOs.

Note: Tiered networks are another aspect to consider. Some states offer these tiered networks, which further classify providers into sub-categories based on cost and quality measures. Opting for preferred providers within these tiers can even lower cost-sharing responsibilities.

Cost Considerations

It’s not a secret that health care is an immense expense for both employers and employees. Both PPOs and EPOs have their own unique cost considerations. PPOs generally have higher monthly premiums and out-of-pocket costs in exchange for increased flexibility and coverage for out-of-network services. That being said, staying in-network for treatment can help keep costs lower than pursuing out-of-network physicians. EPOs tend to have significantly lower monthly premiums and lower out-of-pocket costs.

To help find the right fit for them and their families, employees need to consider how often they anticipate anyone on their plan needs to see doctors other than their primary care physician. If they have chronic conditions and need to see doctors who are out of network, a PPO might be worth the extra cost. For those who visit the doctor infrequently, the reduced cost they encounter each month for premiums tends to make an EPO a more attractive option.

On the employer side, EPOs cost less, but giving employees PPO and EPO options is a great way to ensure that they can take their health care needs into their own hands in whichever way they see fit.

Tax Implications for Companies

Providing employees with access to quality health care plans can help keep a workforce happy and healthy. While this is a major financial investment for businesses, it might save a company some money in the process thanks to the Small Business Health Care Tax Credit.

This tax credit can cover up to 50% of the premiums a business pays for its employees (35% for non-profits) for two consecutive years. To claim this tax credit, businesses must enroll in a Small-Business Health Options Program, or SHOP, plan. Applicable businesses must have fewer than 25 full-time equivalent employees, with an average employee salary of around $56,000 or less per year. They also need to pay at least 50% of full-time employees’ premium costs and offer SHOP coverage to all full-time employees (Coverage for dependents or part-time employees working less than 30 hours per week is not required.)

Plan Flexibility

An EPO may be flexible enough for some, but for others, a PPO will be necessary to simplify the management of their health. Not having to seek referrals can be a big time saver and is a major perk associated with having a PPO. For example, if someone wants to see a dermatologist annually, they likely don’t want to have to jump through hoops each year just to get an annual check-up or a refill for their favorite acne medication.

Choosing the Right Plan For Your Needs

As an employer, selecting the right health insurance plan for employees is crucial. Choosing between a PPO and an EPO can significantly impact costs and employee satisfaction. Read on for a couple of real-life scenarios to help make this informed choice:

Scenario 1: A Diverse Workforce

Overseeing a company with a diverse workforce may impact this decision. Some employees may be young and healthy, while others might have families or chronic health conditions requiring frequent medical attention. A PPO plan might be the better option here. PPOs offer flexibility, allowing employees to choose from a wider range of health care providers, including those out-of-network. This flexibility can be particularly advantageous for those needing specialized care or having pre-existing relationships with certain providers.

Scenario 2: Tight Budget Constraints

Consider another scenario where a company is operating under tight budget constraints. Here, an EPO plan may be more suitable. EPOs typically have lower premiums compared to PPOs and can still provide comprehensive coverage as long as employees stay within the network. This can help manage overall health care costs while still providing substantial employee benefits.

Who Should Choose a PPO Plan?

When considering a PPO plan, think about the level of flexibility and convenience needed. PPOs are especially appealing for those who prefer having a wide range of choices when it comes to health care providers. With a PPO, an individual is not restricted to a specific network and won’t need referrals to see specialists. This can be a significant advantage if they often require specialized medical attention. Moreover, PPO plans are a sensible choice for those who frequently travel or have family members living in different areas. The ability to receive care both within and outside the network means they aren’t limited geographically. While this flexibility comes at a cost, it can be worth it for the ease and freedom it provides. If an individual needs to re-enroll in a new plan and continued access to a prior set of doctors and specialists who are familiar with their medical history is important to them, a PPO plan could be the right fit. They are well-suited for individuals and families who prioritize the convenience of accessible, diverse medical care options over the potential extra expense.

Who Should Opt For an EPO Plan?

For those looking for lower premiums who don’t mind sticking to a network of providers, an EPO might be a great choice. EPO plans work well for individuals who prefer controlled costs and a moderate level of provider flexibility. If someone doesn’t expect to need a wide range of specialists—who may be out-of-network—the limitations of EPOs may not be a problem. Additionally, if they usually stay within the same geographic area where their network providers are located, an EPO can offer sufficient coverage without the higher cost of a PPO. On the other hand, if a person needs frequent out-of-network care or prefers a wide range of healthcare providers, an EPO may not offer the flexibility you need. Nevertheless, for many people, the cost savings and straightforward structure can make EPOs a practical choice for health insurance.

FAQs: Common Questions About PPO and EPO Plans

Q: Can I see any doctor with a PPO plan?

A: Yes, one of the biggest advantages of a PPO plan is its flexibility. You can see any doctor or specialist you choose, even if they are out-of-network. However, you will pay less if you stick to in-network providers.

Q: Do EPO plans require referrals to see specialists?

A: No, unlike HMO plans, EPO plans do not require you to get a referral to see a specialist, as long as the specialist is within the network.

Q: What happens if I go out of network with an EPO?

A: With an EPO, you are responsible for all the costs if you go out of network. EPO plans only cover in-network services, except in emergencies.

Q: Are PPO plans more expensive than EPO plans?

A: Generally, yes. PPO plans tend to have higher premiums compared to EPO plans due to the greater flexibility and larger provider networks they offer.

Q: Which plan offers better coverage for frequent travelers?

A: A PPO plan might be more suitable for frequent travelers since it covers out-of-network care. This can be handy if you need medical assistance while away from home and cannot access in-network providers.

Q: Can I switch from an EPO to a PPO plan?

A: This depends on your insurance provider’s policies and enrollment periods. Typically, you can switch during the open enrollment period or if you qualify for a special enrollment period due to a qualifying life event.

Q: Do PPO plans cover preventative care services?

A: Yes, most PPO plans cover preventive care services like annual check-ups, immunizations, and screenings. However, specifics can vary, so it’s best to check your individual plan details.

Making the Right Choice

Choosing between PPO insurance and EPO insurance ultimately depends on each employee’s individual needs and preferences. If they highly value the freedom to choose their health care providers and are willing to pay higher premiums for that flexibility, a PPO plan may be the better option for them. On the other hand, if this isn’t a primary concern, an EPO plan may suit their needs better.

If you’re looking for more detail on PPO vs HMO plans, check out our article on PPOs vs HMOs.

This story was produced by Thatch and reviewed and distributed by Stacker.