Why did your homeowners insurance go up?

Dontree_M // Shutterstock

Why did your homeowners insurance go up?

Person calculating interest rates with a house figure on the side.

Around a month before homeowners insurance renewal, your insurer will notify you of any changes to your coverage or rates for the coming year. If you saw an increase in rates, you’re not alone. Home insurance premiums were up an average of 21%, according to a Policygenius analysis of policy renewals from May 2022 to May 2023. For homeowners whose premiums went up, the average increase was $244 per year. Find out why this happened and what you can do to lower your premiums.

Seven Reasons Why Your Home Insurance Rates Went Up

If you’re one of the 94% of homeowners who renewed their policy last year just to find out your home insurance rates went up, here are a few reasons why this might have happened.

1. Increase in wildfires, tornadoes, hurricanes, and other natural disasters

Worsening hurricanes in Florida, rampant wildfires out West, devastating tornadoes in the Heartland, and unexpected cold snaps in Texas have caused record-setting claim payouts and financial losses in the home insurance industry. As a result, many insurance companies are increasing rates to pay for these losses and to ensure they don’t go bankrupt after future climate disasters.

As of October 2024, the U.S. has seen 20 billion-dollar disasters this year. According to the National Oceanic and Atmospheric Administration, the average number of billion-dollar disasters from 1980 to 2023 was 8.5 per year, but from 2019 to 2024 the average is 20.4 events.

But it isn’t just homes at risk of hurricanes or wildfires that are paying more for insurance. In fact, several states with the highest average rate increases at renewal in the last few years are in the middle of the country—largely due to the higher incidence of hail and wind damage claims in those states.

As climate change continues to alter weather patterns all over the country, certain areas that insurers used to consider to be low risk are now viewed as the opposite, and homeowners in these areas may suddenly be seeing steep premium hikes as a result.

2. Fewer carriers are willing to write policies in high-risk states

When there are fewer insurers left to choose from in a particular state or region, the ones remaining will often implement stricter underwriting criteria and increase costs to reflect both the higher demand and exposure, resulting in higher premiums for homeowners. This trend continues in high-risk states like Florida and California.

Just last year, Allstate and State Farm stopped writing new policies in California, Farmers placed a cap on how many new policies it would write in the Golden State, and Safeco dropped around 1,000 policies in the Bay Area.

The same goes for Florida, where as many as 10 companies have already gone insolvent since 2020. Last year, AAA announced it would not renew home insurance policies in “higher-exposure” areas of Florida, and Farmers announced it would stop writing new policies and won’t renew thousands of existing ones. This is on top of Progressive, AIG, and Heritage, all of which had already announced they were no longer writing new policies in Florida.

3. Increase in supply chain issues and the cost of building materials due to inflation

Home insurance premiums have gone up everywhere due to the increased cost of labor and construction materials, thanks to supply chain issues and high inflation that started in 2020 and has persisted until today.

Your rates are based heavily on how much dwelling coverage is in your policy—this is the part of your home insurance that pays to rebuild your home if it’s damaged. Higher rebuild costs due to inflation means homes are requiring higher dwelling coverage limits to keep up with the rising prices.

This has led to higher home insurance rates across the board. While lumber and wood construction materials have tapered off since reaching highs in 2022, prices remain high compared to before the pandemic. Costs of material goods for new residential construction, and asphalt roofing materials also remain high, according to the Bureau of Labor Statistics.

The labor shortage in the construction industry also remains a problem for insurers—and in turn, homeowners. There were 368,000 construction job openings as of August 2024—38,000 more than July and more than double the number expected by the Bureau of Labor Statistics.

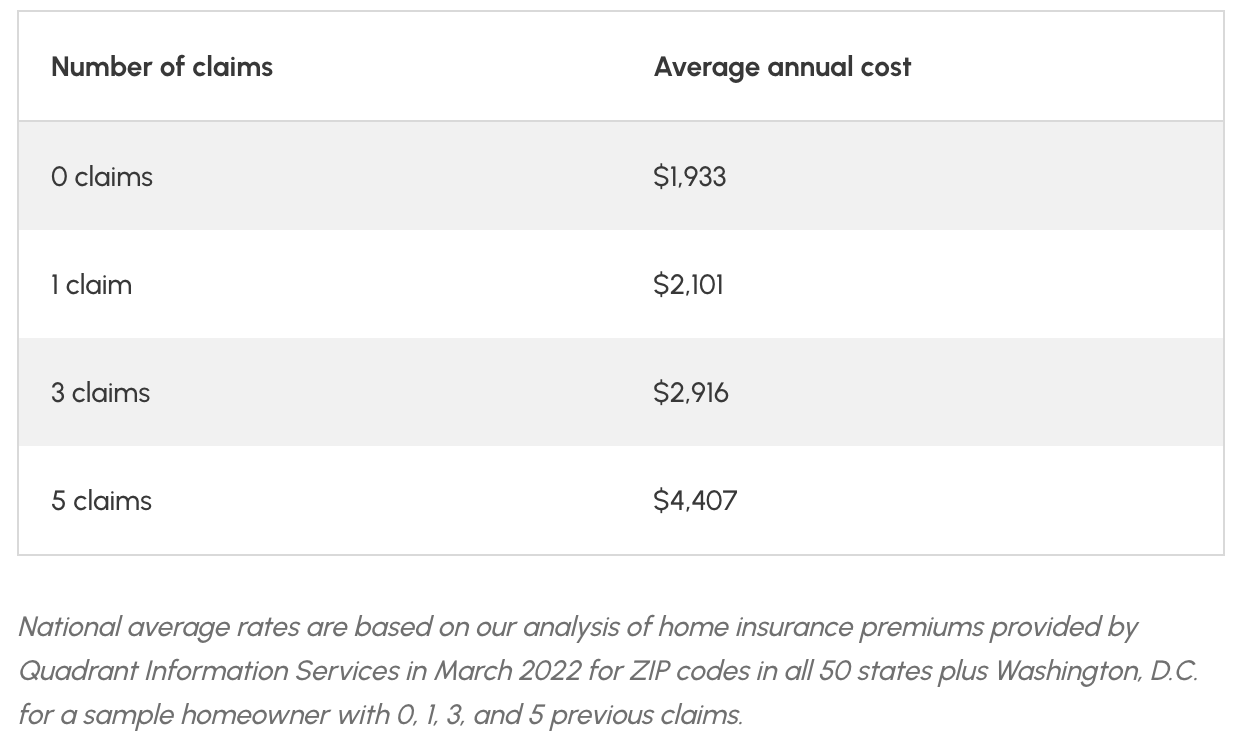

4. You filed a claim or multiple claims last year

Another factor that determines your home insurance rates is your likelihood of filing a claim. Insurers view claims related to theft, water damage, and liability as more likely to be repeated than others, so they’ll often increase premiums after just one of these claims due to that higher risk.

On average, home insurance premiums increase roughly 7% to 10% after a claim, according to Fabio Faschi, former Property and Casualty Lead at Policygenius. So if you filed a claim or two recently, that may be the reason why your homeowners insurance went up.

![]()

Policygenius

Average Cost of Home Insurance After You File a Claim

Table showing the average annual cost of home insurance in 2022 by claim history.

See the average annual cost of home insurance in 2002 by claim history in the table above.

5. Your roof is old and due to be replaced

If your roof is around 10 or 15 years old, your home insurance company may start raising your rates each year to offset the risk of you filing a claim. The reason for this is your roof—along with your home’s systems and foundation—is what keeps your house intact.

Once your roof starts showing signs of deterioration, that’s a telltale sign to insurers that it’s only a matter of time before it’s damaged—especially if you live in areas at high risk of windstorms or hail.

6. Your credit score went down last year

Insurance companies run their own version of a credit check to determine how much of a risk you are to insure. Homeowners with bad credit are considered more likely to file a home insurance claim, and so you’ll pay higher insurance rates as a result of this.

This is because insurers assume if you have good financials and a good credit score, you’re staying on top of your insurance payments and maintaining the property—making necessary house repairs and upkeep. A bad storm will probably pose less of a risk to a home that’s well taken care of and structurally sound than one that isn’t.

On the flip side, homeowners with a poor credit score are more likely to have outstanding debt and are viewed as more likely to depend on an insurance payout in the event that something bad happens.

So if your credit score took a dip over the last year, you’ll likely pay for it in higher home insurance rates.

7. You added a pool, trampoline, or other “attractive nuisance” to your home

Insurance companies consider swimming pools, trampolines, and even house pets as “attractive nuisances” since they attract children onto your property and put them at risk for injury.

If you install a pool or add a new four-legged friend to your family, your insurance company may increase your rates to offset the higher probability of expensive liability claims.

Three Ways to Lower Your Homeowners Insurance Rates

If you noticed your home insurance rates went up recently, here are a few tips to help you save.

Ask about discounts

If the discounts section on your policy’s declarations page is more or less empty, make sure to ask your insurance company if there are any you are currently eligible for. Some popular discounts include:

- Multi-policy discount: If you have two or more policies with the same insurer, like home and auto insurance, this can trim anywhere from 15% to 30% off your premiums, depending on your insurer.

- Claim-free discount: Some carriers will provide discounts if you go a certain number of years without filing a claim.

- Protective devices discounts: If your home is fitted with deadbolts, smoke detectors, fire extinguishers, fire and burglar alarms, or other protective features, most insurers will reward you with lower rates.

- Loyalty discount: If you’ve been a policyholder with the same insurance company for five years or more, you may be eligible for a loyalty discount of up to 10% off.

Switch to a higher deductible policy

Increasing your policy deductible generally lowers your home insurance premiums. If your rates recently went up and your deductible is currently set to $1,000, consider choosing a higher deductible to get those rates back down.

If your home doesn’t face many hazards or you’ve owned your house a while without having to file a claim, then it may be in your best interest to choose a high-deductible policy.

Re-shop your homeowners insurance

Experts recommend re-shopping your home insurance every year to make sure you aren’t missing out on better coverage or rates with a different insurance company.

This story was produced by Policygenius and reviewed and distributed by Stacker.