Uninsured drivers are on the rise: Are you protected?

chalermphon_tiam // Shutterstock

Uninsured drivers are on the rise: Are you protected?

The National Highway Traffic Safety Administration has reported that the United States experiences millions of motor vehicle accidents every year. Driving is an inherently risky activity, with personal injury and property damage being some of the most common consequences. To reduce the financial burden that comes with these consequences, auto insurance is mandatory in most states. Despite this, millions of vehicles on the road today are uninsured, and this number is only growing.

According to the Insurance Research Council, 15.4% of U.S. drivers in 2023 were completely uninsured, up 3% from 2017. As a result, you could be the one footing the repair bill the next time you get into an accident, even if it was no fault of your own.

CheapInsurance.com examines where uninsured motorists are most common, why it occurs, and what drivers can do to protect themselves.

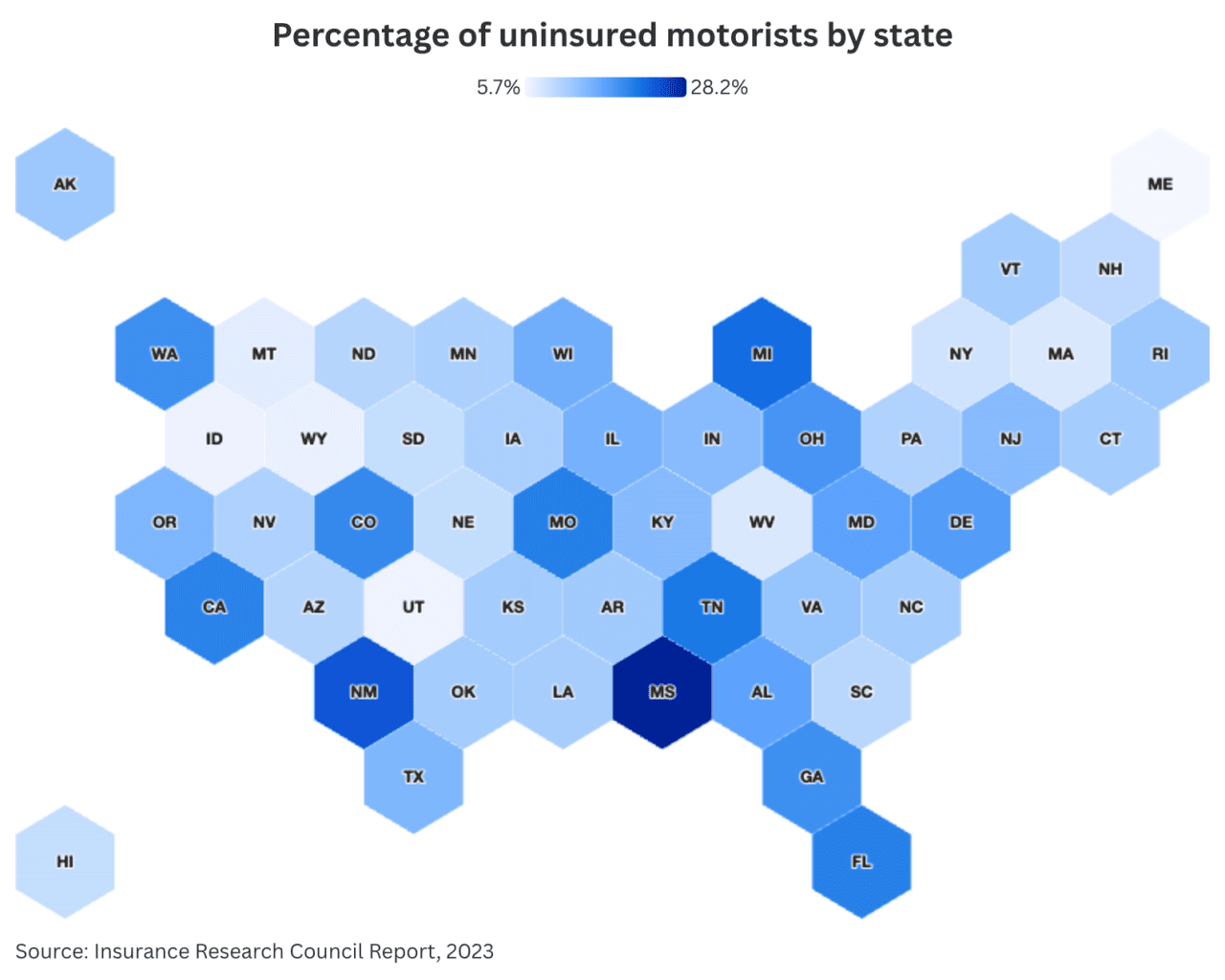

Highest and lowest uninsured motorists by state

The levels of uninsured drivers vary from state to state. Overall, Mississippi, New Mexico, and Michigan have the highest rates. Maine, Utah, and Idaho are the three lowest. Here’s a complete breakdown of uninsured drivers by state, based on data from the Insurance Research Council’s 2025 report, which examines 2023 data.

CheapInsurance.com

Top 10 states by percentage of uninsured motorists

- Mississippi (28.2%)

- New Mexico (24.1%)

- Michigan (22.3%)

- Tennessee (21.3%)

- Missouri (20.7%)

- Florida (20.6%)

- California (20.4%)

- Colorado (19.7%)

- Washington (19.1%)

- Georgia (19%)

Bottom 10 states by percentage of uninsured motorists

- Maine (5.7%)

- Utah (6.2%)

- Idaho (6.4%)

- Wyoming (6.7%)

- Montana (7.2%)

- West Virginia (7.8%)

- Massachusetts (7.9%)

- New York (8.6%)

- South Dakota (9.4%)

- Nebraska (9.5%)

Why do people drive uninsured?

There are legal, social, and economic reasons why some drivers forego having auto insurance. Some people are not required to have insurance, some face barriers to getting it, and some cannot afford it.

New Hampshire is the only U.S. state where car insurance is not mandatory for drivers. In states where it is required, the dollar amount of bodily injury liability per person, per accident, and property damage liability can vary.

Socially, some individuals face barriers to getting car insurance and may not even be able to obtain it. For example, those with a poor driving history (multiple collisions or DUI convictions) or those with a record of insurance fraud may find it challenging.

Financially, many people struggle to afford car insurance and may choose to go without it as a result. In fact, a 2024 industry report from Deloitte reported that up to 45% of young Americans have considered going without insurance because of rising costs. Due to how insurance premium pools work, the cost will only go up as more people skip coverage. Many of the most expensive states for car insurance also experience the highest number of uninsured drivers.

Issues with enforcement

Enforcement can vary across jurisdictions. In some states, harsher punishments apply, such as hefty fines, jail time, and license suspension. In many others, such as Connecticut, the punishments are negligible and include “no action,” “verbal warning,” “written warning,” a ticket, or a misdemeanor.

The risks that insured drivers face

Uninsured drivers pose a substantial risk to insured drivers on the road, mainly financial. If a driver experiences a no-fault accident with a driver who does not have insurance, their damages may have to be covered by their own insurance company or out of pocket. While drivers can go after an uninsured driver through a lawsuit, the potential legal costs can outweigh the settlement.

Some of the key financial risks that drivers face from uninsured motorists include the following.

- Property damage costs: If a person’s vehicle is damaged in an accident by a driver without insurance, they will not be able to file a claim with the insurer of the driver responsible for the accident. This often means that they must go through their own insurance company and file a claim.

- Bodily injury costs: Personal injury is a real possibility for many accidents. A person may be forced to pay their own medical bills if hit by an uninsured driver. Even in the case of a lawsuit, it may take six months to a year to get a payout.

- Higher insurance premiums: If a person has to use their own comprehensive insurance to file a property damage or bodily injury claim, they may face higher premiums in the future, even if they were not at fault.

Avoiding risk: Insurance strategies to consider

Fortunately, there are ways to reduce the financial risk one faces from uninsured drivers on the road. Many auto insurance companies offer a supplemental add-on called uninsured/underinsured motorist coverage.

Uninsured motorist (UM) coverage protects drivers against any personal injury costs associated with the accident. Underinsured motorist (UIM) coverage pays the difference between how much the personal injury costs were and how much the at-fault party’s insurance was willing to cover.

Most of the time, optional UM/UIM insurance only covers personal injury. Uninsured motorist property damage (UMPD) is another add-on that an insurer can provide. This will cover any costs associated with the repair of a damaged vehicle.

How to expand coverage to protect against uninsured drivers

The simplest way for a person to get UM/UIM coverage is to contact their auto insurance company; however, the availability can depend on the state. In around 20 jurisdictions, it’s mandatory to have UM coverage, whereas in others, it’s just a requirement that it’s offered to the customer. UIM coverage is less common and is only required in a small selection of states.

While adding this type of insurance doesn’t help curb the problem of the growing number of uninsured drivers, it does reduce the risk for those who have coverage.

Staying protected against uninsured drivers

The increasing occurrence of uninsured driving across the country highlights the importance of understanding the risks and available protections. Until the social and economic factors driving this trend change, the number of uninsured drivers is unlikely to decrease.

Supplemental uninsured motorist insurance can mitigate the financial risks associated with sharing the road with drivers who do not have coverage, offering financial security in the event of a no-fault accident or personal injury.

This story was produced by CheapInsurance.com and reviewed and distributed by Stacker.

![]()