Gen X, millennials pay more for their mortgages

Natee Meepian // Shutterstock

Gen X, millennials pay more for their mortgages

Millenial couple calculating mortgage and expenses.

The average mortgage payment in the U.S. has risen sharply since 2020 for every generation except baby boomers, a clear side effect of still-elevated mortgage interest rates and home prices hovering near all-time highs. While longtime homeowners haven’t seen much motion in their payments since 2020 thanks to fixed interest rates, newer (and oftentimes younger) homebuyers have borne the brunt of recent disruptions in the market.

According to Experian data from the second quarter of 2024, millennials carry the highest average mortgage balance of any generation. And while Generation X still tops their average monthly mortgage payment, millennials are on track to eclipse them in the near future.

But before projecting what might happen next in the mortgage market, Experian takes a look at the current housing landscape that current mortgagees are facing, and how that may affect their next housing move (which, in turn, may impact the rest of those still looking for a way in).

![]()

Experian

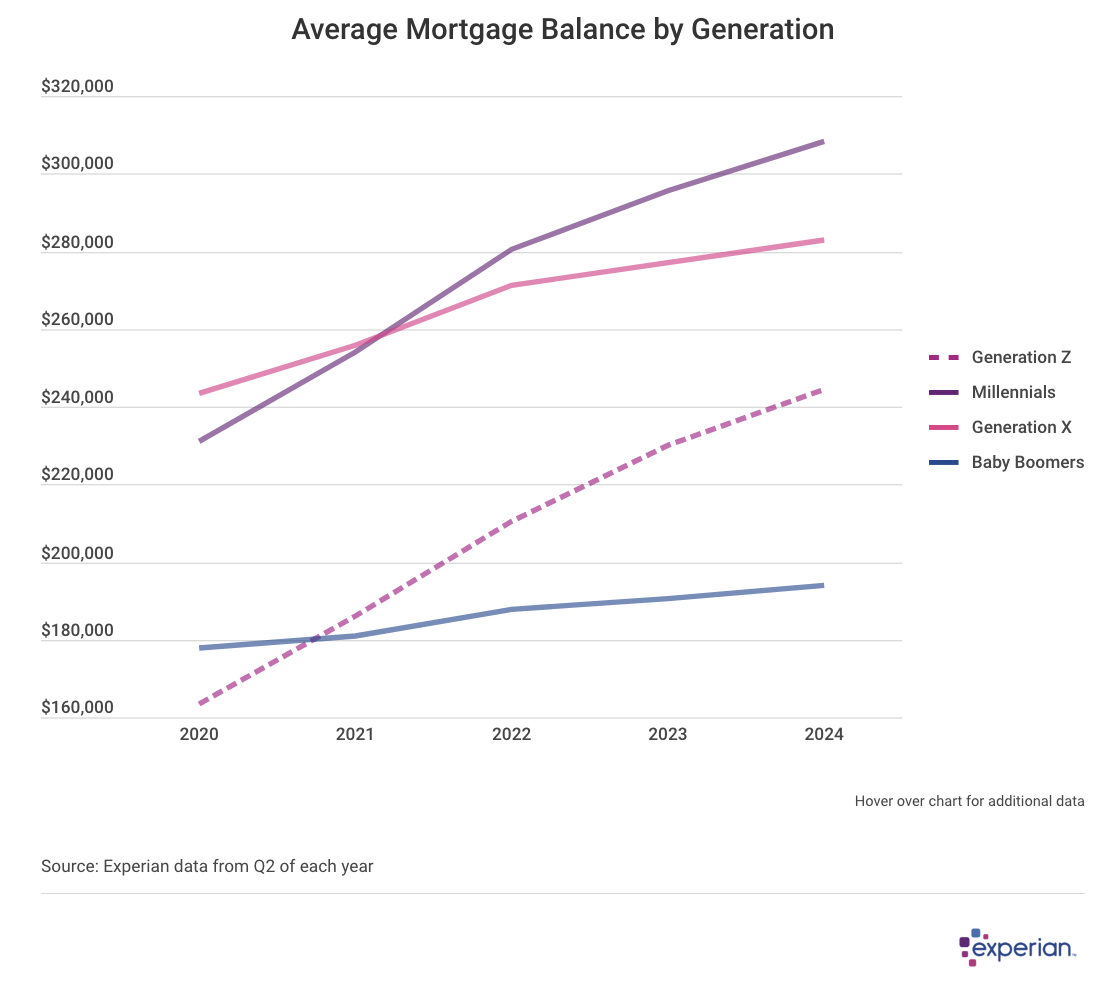

The Balances of Power in the Mortgage Market

Line graph showing “Average Mortgage Balance by Generation”.

Since 2020, millennials have swapped places with their older counterparts in Generation X and now carry—by far—the largest average mortgage balances of any other generation. At $308,000, the millennial generation has an average mortgage balance that’s nearly $25,000 larger than that of Gen X, the generation that had the biggest balance in 2020.

Meanwhile, the few buyers of Generation Z who secured a mortgage since 2020 now owe an average of more than $244,000 on their mortgage. That total is nearly 50% higher than in 2020, when a few very young consumers found a very few number of homes to buy and finance.

Finally, baby boomers more or less owe similar amounts on their mortgages since 2020, and only owe an average of $193,000 on their mortgages in 2024, nearly 40% less than millennials.

Interestingly, those levels don’t exactly carry over to the monthly payments each generation is responsible for. In this case, Generation X pays slightly more than millennials toward their mortgages each month, but both pay around $2,300 per month, on average. Those much older or younger than the two middle generations pay significantly less in mortgage payments: Gen Z has an average mortgage payment of $1,882 each month, while baby boomers pay even less: $1,724 monthly as of June 2024.

Experian

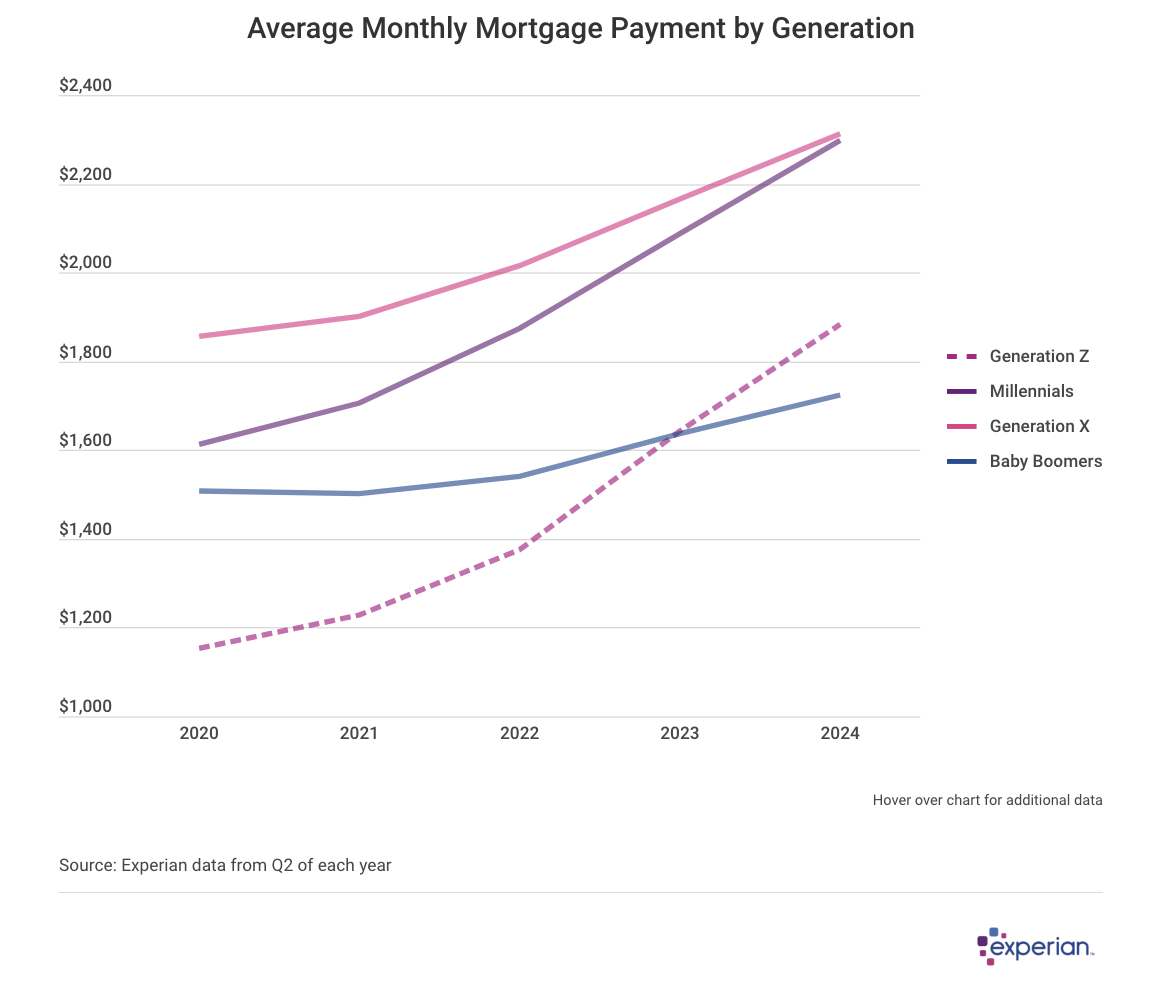

Several Factors Influence Monthly Mortgage Payments

Line graph showing “Average Monthly Mortgage Payment by Generation”.

While there may appear to be a bit of a disconnect between average mortgage balance and average monthly mortgage payment data, consider all the variables that comprise the monthly payment calculation: The terms of the mortgage, the interest rate, and the amount of equity the borrower has in their mortgaged property all feed into average mortgage repayment figures.

Let’s look at term impact first. While most mortgages are paid over a period of 30 years, some have shorter terms. Fixed-rate loans with 15-year terms, for instance, were especially popular among some home borrowers a few years ago, as borrowers realized they could pay off their mortgage faster at lower interest rates—albeit with a slightly higher monthly payment.

The year the mortgage was made—also known as its vintage—is another factor impacting the interest rates each generation pays on their current mortgages today.

In addition, adjustable rate mortgages, while largely out of vogue last decade, have become a more popular alternative to the 30-year fixed-rate mortgage as monthly interest rates have climbed.

Finally, younger homeowners who purchased their home recently are more likely to be paying a higher interest rate than those in older generations who were approved for their mortgage before rate hikes increased to a 21st-century high beginning in 2022.

There is some good news for would-be homebuyers, however. Even prior to the September 2024 rate cut by the Federal Reserve (the first of what are expected to be several), mortgage rates had been falling. As September came to a close, the average 30-year fixed rate conventional mortgage rate was 6.08%, according to Freddie Mac, nearly a full percentage point lower than at the beginning of the year.

Refinancing Booms and Busts

Let’s not forget mortgage refinancing: the process of renegotiating the interest you’ll pay on any remaining mortgage balance. Throughout the 2010s, multiple waves of refinancing occurred among existing homeowners, as mortgage rates fell from 6% to 5% to 4%, and then finally below 3% in 2020.

The result is, for each generation, a blend of inputs of rates and prices. While Experian doesn’t have complete information on loan terms—lenders report if payment amounts were made, not the terms or the interest rates—some general inferences can be made based on when each generation was buying their homes.

- Baby boomers are coasting on lower rates fuelled by refinancing and home equity. Nearly two-thirds of boomers with a mortgage have one that’s refinanced, according to Freddie Mac calculations. They’re also the generation with the most home equity, the fewest average number of years remaining on their mortgage, and make the lowest monthly payments. While some of these enviable conditions are a function of longevity, fortuitous timing is likely as much of a factor, especially considering the next-oldest generation.

- Generation X still has the highest monthly payments. At an average monthly mortgage payment of $2,313, their typical payment exceeds even those of millennials, who have higher average mortgage balances. Household size explains part of this: Gen X families are more likely to have children and less likely to be single-person households than younger homeowners, so their properties will have larger footprints.

- Mortgages are a big lift for most current millennial homeowners. However, with an average monthly mortgage payment of $2,283, according to Experian data, current millennial homeowners may still have an advantage over renters who make similarly sized housing payments and build no equity to show for it. Properties are scarce, especially for entry-level homes; prices remain elevated and 30-year mortgage rates are still above 6%, even after the Federal Reserve rate cuts beginning in September 2024.

- Generation Z homeowners are just starting out. Currently, only 3% of homeowners with a mortgage are under age 28, according to Experian data. And their relatively modest balances averaging $244,000 in June 2024 result in relatively more modest mortgage payments of $1,883 monthly—nearly $400 less than the next two older generations.

Experian

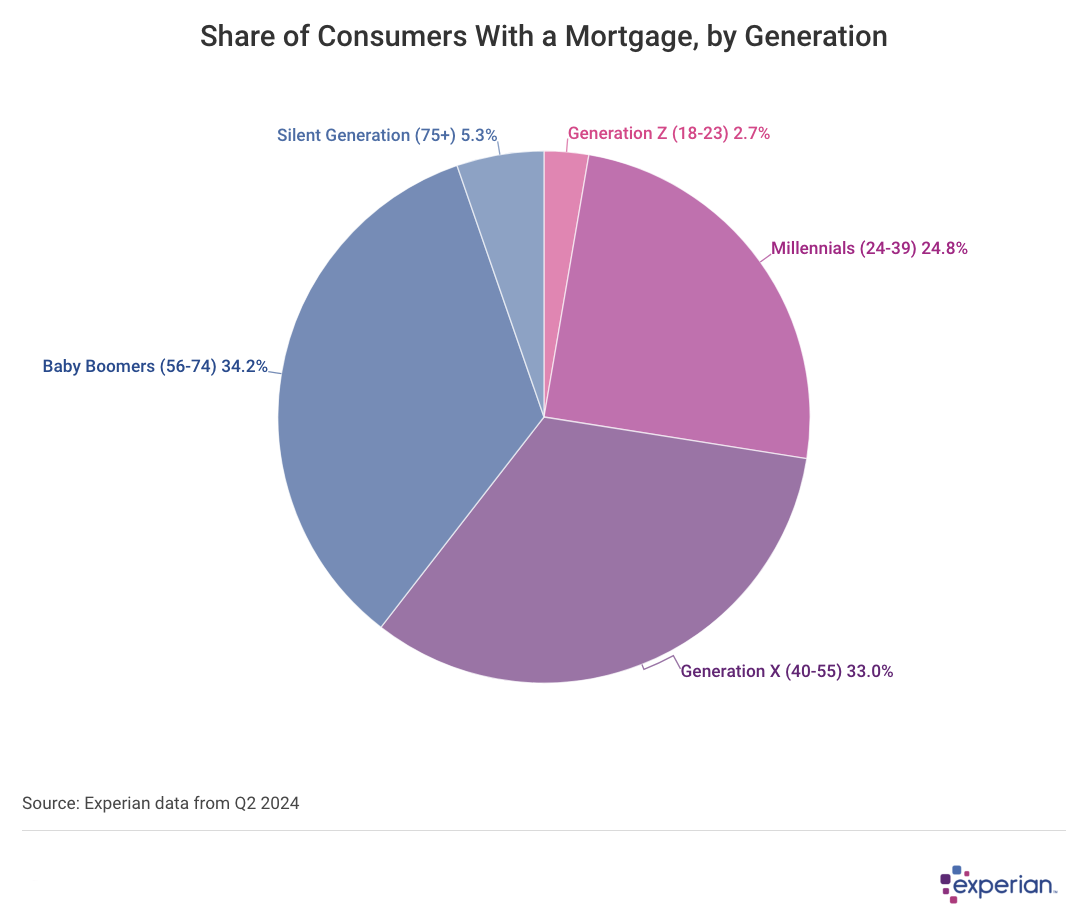

Ownership Remains Elusive for Many

Pie chart showing data on “Share of Consumers With a Mortgage, by Generation”.

Unfortunately, recent drops in rates won’t be enough on their own to get the For Sale signs up and home prices down. Other dynamics in play are effectively sidelining even the most eager of homebuyers in 2024. Those factors include the subdued rate that new homes were being built, the number of cash-only home sales, and (perhaps most importantly) the price of a new mortgage.

Additionally, all-cash purchases still feature prominently in residential real estate transactions, with well over a quarter of home transactions not involving a mortgage. All other things being equal, sellers will prefer a buyer with no mortgage required to close—a process that can add weeks to a residential real estate transaction.

Although a large percentage of home purchases are still being financed with a mortgage, housing inventory remains thin. It’s estimated that, depending on the source, there’s a deficit of between 1.5 million and 5.5 million residential units in the U.S. Even with all the need for new housing, homebuilders are still working at a rate that, while historically healthy, still isn’t making much of a dent in the national housing shortage.

Having fewer homes for sale potentially excludes not only renters who are ready to buy, but also homeowners who are ready to sell their current home to buy elsewhere. Fewer sales in the residential real estate market also mean a larger percentage of sales will be of new construction, which is more abundant in some parts of the country than others.

The Bottom Line

Lower mortgage rates are a start, and could kick-start a cycle of current homeowners finally being able to trade up or down, resulting in more vacated homes for resale and more new homebuyers. And additional rate cuts may finally be able to provide relief to some current homeowners: those with either mortgage APRs above 5% or the few homeowners currently paying adjustable rate mortgages.

However, if increased demand for construction workers, equipment, and materials needed for new home construction ignites another round of inflationary pressure, the Federal Reserve could quickly put the brakes on any additional rate reductions. Regardless of interest rate policy, demographics will still be destiny for many current and would-be homeowners in any future economic environment.

This story was produced by Experian and reviewed and distributed by Stacker Media.